DINAMIKA DISPERSIJE DOHOTKA U EVROPSKOJ UNIJI NAKON GLOBALNE FINANSIJSKE KRIZE

Apstrakt

Ova studija ispituje dinamiku disperzije dohotka među državama članicama Evropske unije tokom postkrizne decenije. Fokusirajući se na period od 2010. do 2019. godine, analiza istražuje da li su se razlike u dohotku među ekonomijama EU smanjile nakon globalne finansijske krize. Korišćenjem godišnjih podataka za 27 država članica EU, procenjuje se sigma-konvergencija praćenjem kretanja međusobne disperzije realnog BDP-a po glavi stanovnika. Rezultati ukazuju na statistički značajno smanjenje disperzije dohotka tokom posmatranog perioda, što sugeriše prisustvo sigma-konvergencije. Međutim, dodatne panel procene ne pružaju dokaze o uslovnoj beta-konvergenciji nakon uključivanja strukturnih kontrolnih varijabli. Ovi nalazi ukazuju da uočeno smanjenje disperzije može odražavati šire mehanizme makroekonomskog prilagođavanja, a ne sistematski proces sustizanja zemalja sa nižim nivoom dohotka. Rezultati doprinose literaturi o evropskim integracijama isticanjem razlike između dinamike disperzije i konvergencije zasnovane na ekonomskom rastu u postkriznom okruženju.

Članak

1. Introduction

The question of income convergence has remained central to modern growth theory and empirical macroeconomics for several decades. Within the neoclassical framework, economies are expected to converge toward their steady-state income levels conditional on structural characteristics such as savings rates, human capital accumulation, and population growth (Barro & Sala-i-Martin, 1992, 2004). Empirical testing of β-convergence, particularly through panel estimations that control for country-specific heterogeneity, has provided evidence of conditional convergence within relatively homogeneous groups of economies (Islam, 1995). However, the magnitude, speed, and stability of convergence have proven sensitive to sample composition, institutional heterogeneity, and the broader macroeconomic environment.

Subsequent theoretical contributions introduced the possibility of multiple steady states and threshold effects, suggesting that convergence may occur within structurally similar groups while divergence persists across broader samples (Azariadis & Drazen, 1990; Durlauf & Johnson, 1995). This perspective has motivated empirical investigations into convergence clubs and the role of institutional and structural characteristics in shaping long-run development paths. In the European context, convergence has been closely linked to economic integration, market liberalization, and institutional harmonization following successive waves of enlargement.

The European Union provides a particularly relevant setting for examining convergence dynamics. The process of economic integration has been accompanied by structural reforms, fiscal coordination, monetary integration, and regulatory harmonization. Earlier empirical studies documented evidence of income convergence among EU member states, especially during the pre-crisis expansion period (Barro & Sala-i-Martin, 1992; Barro & Sala-I-Martin, 1997). However, the global financial crisis and the subsequent sovereign debt crisis fundamentally altered macroeconomic conditions within the Union. The post-2008 environment was characterized by asymmetric shocks, fiscal consolidation, divergent recovery speeds, and persistent productivity challenges, raising renewed questions about the sustainability of convergence within the EU.

While much of the literature has focused on β-convergence — examining whether lower-income economies grow faster than higher-income ones — less attention has been devoted to dispersion-based measures of convergence in the post-crisis decade. Sigma-convergence, defined as a reduction in cross-sectional income dispersion over time, offers a complementary perspective by directly tracking inequality across countries rather than relying solely on growth regressions. Importantly, σ-convergence may occur even in the absence of β-convergence, particularly when macroeconomic adjustment mechanisms compress income differences without systematic catch-up growth.

The present study examines income dispersion dynamics within the European Union during the period 2010–2019, corresponding to the post-crisis decade preceding the COVID-19 shock. Using annual data for 27 EU member states, we analyze the evolution of cross-sectional dispersion in real GDP per capita and assess whether income differences narrowed over this period. In addition, we estimate standard panel growth specifications to evaluate whether dispersion dynamics are accompanied by conditional β-convergence once structural controls are included.

By focusing on the post-crisis decade, this study contributes to the literature in two ways. First, it isolates a macroeconomically distinct period characterized by slower growth, fiscal consolidation, and structural adjustment, thereby allowing for a clearer assessment of convergence under constrained economic conditions. Second, it highlights the distinction between dispersion-based convergence and growth-based convergence, emphasizing that declining income inequality across countries does not necessarily imply systematic catch-up dynamics.

The findings suggest that while income dispersion across EU member states declined during the examined period, conditional β-convergence is not robustly supported once structural controls and fixed effects are introduced. These results underline the importance of distinguishing between different convergence concepts and provide insight into the nature of economic adjustment within the European Union following the global financial crisis.

2. Literature Review

The empirical investigation of income convergence has remained a central theme in growth economics since the formalization of the neoclassical convergence hypothesis. Early cross-country studies provided systematic evidence of conditional β-convergence, demonstrating that economies with similar structural characteristics tend to converge toward comparable steady states once differences in savings, human capital accumulation, and population growth are controlled for (Barro & Sala-i-Martin, 1992, 2004). Panel data approaches further strengthened these findings by accounting for unobserved heterogeneity and country-specific effects (Islam, 1995), thereby refining the empirical foundations of convergence analysis.

Subsequent theoretical and empirical developments challenged the assumption of a unique steady state. Models incorporating multiple equilibria and threshold effects emphasized the possibility of heterogeneous convergence paths across structurally distinct groups of economies (Azariadis & Drazen, 1990; Durlauf & Johnson, 1995). This perspective encouraged the empirical exploration of convergence clubs and the recognition that convergence may be conditional not only on economic fundamentals but also on institutional and structural characteristics. The introduction of time-varying factor models and the log-t test further advanced the methodological toolkit by allowing for heterogeneous transitional dynamics and endogenous club formation (Phillips & Sul, 2007, 2009).

Within the European context, convergence has been closely linked to the broader process of economic integration and institutional harmonization. Enlargement waves and deepening integration were expected to facilitate catch-up growth through capital mobility, regulatory alignment, and access to common markets. Empirical studies conducted during the pre-crisis expansion period generally documented evidence of convergence among EU member states, particularly between new and old members during the early years of accession. However, the global financial crisis and the subsequent sovereign debt crisis fundamentally altered macroeconomic conditions within the Union, generating asymmetric shocks, fiscal stress, and divergent recovery trajectories.

The distinction between β-convergence and σ-convergence has gained increasing importance in this context. While β-convergence examines whether lower-income economies grow faster than higher-income ones, σ-convergence focuses on the evolution of cross-sectional income dispersion over time. A reduction in dispersion indicates convergence in distributional terms, even if growth regressions do not reveal systematic catch-up dynamics. Importantly, β-convergence is a necessary but not sufficient condition for σ-convergence, and the two measures may diverge during periods characterized by structural stagnation or asymmetric adjustment. In mature economic unions, dispersion may decline due to slower growth in advanced economies rather than accelerated growth in lower-income members.

Recent empirical contributions have emphasized that post-crisis European convergence dynamics differ from earlier integration phases. Analyses of income and institutional convergence across EU Core, EU New, and peripheral economies suggest that heterogeneity persists despite formal institutional alignment (Lalić & Trifunović, 2026a). Complementary research highlights that institutional hierarchy and structural positioning within the Union shape differential growth responses, particularly in periods of macroeconomic stress (Lalić & Trifunović, 2026b). Further evidence indicates that crisis asymmetry plays a significant role in shaping convergence outcomes, with peripheral

economies exhibiting greater volatility and weaker adjustment capacity (Lalić & Trifunović, 2026c). More recent work examining nonlinear convergence mechanisms underscores that growth responses may vary across institutional regimes and development stages, suggesting that convergence patterns remain conditional and context-dependent (Lalić & Trifunović, 2026d).

Beyond convergence testing, the broader institutional economics literature provides a conceptual framework for understanding persistent heterogeneity across European economies. Institutions define the incentive structure within which economic activity takes place (North, 1990), while empirical research links governance quality to long-run income levels and productivity performance (Acemoglu et al., 2001; Acemoglu & Robinson, 2012; Rodrik et al., 2004). Although institutional harmonization has been a central objective of European integration, empirical evidence suggests that implementation depth and enforcement capacity vary across member states, influencing growth consistency and resilience.

Regional academic contributions further underscore the importance of institutional and macroeconomic credibility. Analyses of competitiveness indicators in European economies highlight structural constraints linked to institutional capacity (Anufrijev et al., 2026). Recent evidence from the Western Balkans further suggests that differences in competitiveness indicators and labor market structures remain important determinants of long-run development potential and regional economic performance (Anufrijev et al., 2025). Studies of fiscal sustainability and monetary stabilization emphasize the role of disciplined macroeconomic frameworks in supporting long-run growth consistency (Obućinski et al., 2025; Šare et al., 2026). Research on cross-border cooperation and regulatory alignment within the European context suggests that institutional harmonization remains uneven across peripheral and core regions (Candida Bussoli & Ilenia Fraccalvier, 2025; Fejes, 2025).

More broadly, recent analyses of post-crisis European growth patterns indicate that macroeconomic adjustment mechanisms, fiscal consolidation strategies, and structural reforms have played a significant role in shaping cross-country income dynamics (European Commission, 2022). Similar conclusions are reported in studies examining the effects of fiscal policy and public debt dynamics on economic growth, emphasizing the importance of macroeconomic stability for sustainable convergence processes (Šare et al., 2026). The coexistence of monetary integration and divergent fiscal capacities has generated complex adjustment processes, raising renewed questions about the sustainability of convergence within the Union.

Taken together, the literature suggests that convergence within the European Union cannot be assumed to be stable across macroeconomic regimes. The post-crisis decade represents a structurally distinct period characterized by subdued growth, fiscal consolidation, productivity slowdown, and uneven institutional adaptation. In this context, examining σ-convergence provides a direct assessment of whether income disparities narrowed despite the absence of robust catch-up growth dynamics. By focusing on income dispersion during the 2010–2019 period and complementing distributional analysis with panel growth estimations, the present study situates itself within the established convergence literature while addressing the specific institutional and macroeconomic conditions of the post-crisis European environment.

3. Data and Variables

The empirical analysis is based on an unbalanced panel dataset covering 27 European Union member states over the period 2010–2019. The selected time horizon corresponds to the post-crisis decade following the global financial crisis and the subsequent sovereign debt episode, thereby isolating a macroeconomically distinct phase characterized by fiscal consolidation, monetary accommodation, and heterogeneous recovery paths across member states. By focusing on this subperiod, the analysis aims to evaluate income dispersion dynamics under conditions of constrained growth and structural adjustment.

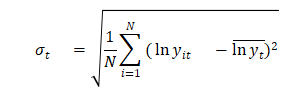

All macroeconomic variables are obtained from the World Bank’s World Development Indicators (WDI), ensuring cross-country comparability and methodological consistency across the entire sample. Real GDP per capita (constant prices) is used as the primary measure of income levels. For the purpose of σ-convergence analysis, the logarithm of real GDP per capita is computed and its cross-sectional standard deviation is tracked annually to assess the evolution of income dispersion across EU member states. A declining standard deviation over time indicates the presence of sigma-convergence.

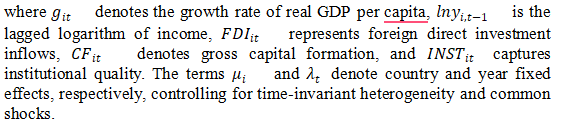

In addition to dispersion analysis, complementary panel estimations are conducted using real GDP growth as the dependent variable in conditional convergence specifications. The baseline explanatory variable is the lagged logarithm of real GDP per capita, which captures the traditional β-convergence mechanism. A negative and statistically significant coefficient would imply that lower-income economies grow faster than higher-income ones, whereas a non-significant or positive coefficient suggests the absence of systematic catch-up dynamics.

Several structural control variables are included in the growth regressions. Foreign direct investment inflows (as a percentage of GDP) are incorporated to capture capital mobility and external financing effects. Given the presence of extreme outliers in FDI series, the variable is winsorized at the 1st and 99th percentiles to mitigate the influence of abnormal capital flow episodes. Gross capital formation (as a percentage of GDP) is included as a proxy for domestic investment intensity and capital deepening. Institutional quality is measured using a composite index derived from the Worldwide Governance Indicators (WGI), which aggregate six governance dimensions - Voice and Accountability, Political Stability, Government Effectiveness, Regulatory Quality, Rule of Law, and Control of Corruption - into a single standardized measure. The institutional index captures cross-country differences in governance capacity and regulatory stability that may condition growth performance.

The dataset comprises 270 country-year observations in the baseline specification, corresponding to 27 EU member states over ten years. While the panel is largely balanced, minor gaps in selected control variables are addressed through sample adjustment in regression estimations. All regression models include country fixed effects to control for time-invariant heterogeneity and year fixed effects to account for common macroeconomic shocks affecting all member states simultaneously.

By combining dispersion-based analysis with panel growth estimations, the empirical framework allows for a distinction between distributional convergence and growth-based convergence during the post-crisis decade. This dual approach ensures that changes in income dispersion are evaluated alongside the structural determinants of growth dynamics within the European Union.

4. Methodology

The empirical strategy combines dispersion-based analysis with panel growth regressions in order to distinguish between sigma-convergence and conditional beta-convergence during the post-crisis decade. This dual approach allows for an assessment of whether declining income disparities reflect systematic catch-up dynamics or broader macroeconomic adjustment mechanisms.

Sigma-convergence is evaluated by examining the evolution of cross-sectional dispersion in real GDP per capita across EU member states. Following the standard definition, sigma-convergence occurs if the dispersion of income levels declines over time. Formally, dispersion is measured as the cross-sectional standard deviation of the logarithm of real GDP per capita:

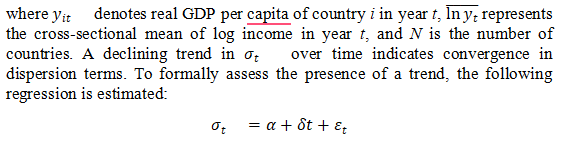

where t represents the time index. A negative and statistically significant coefficient ![]() provides evidence of sigma-convergence.To complement dispersion analysis, conditional beta-convergence is examined using a fixed-effects panel regression framework. The baseline specification is given by:

provides evidence of sigma-convergence.To complement dispersion analysis, conditional beta-convergence is examined using a fixed-effects panel regression framework. The baseline specification is given by:

Within this framework, beta-convergence is supported if the coefficient β\betaβ is negative and statistically significant, indicating that lower-income economies grow faster than higher-income ones after controlling for structural factors. Conversely, a non-significant or positive coefficient suggests the absence of systematic catch-up growth.

All panel estimations are conducted using two-way fixed effects. Standard errors are clustered at the country level to account for heteroskedasticity and

serial correlation within cross-sectional units. As a robustness check, Driscoll–Kraay standard errors are also estimated to address potential cross-sectional dependence in macro-panel settings. The empirical analysis therefore allows for a comprehensive evaluation of convergence dynamics while maintaining econometric robustness.

By combining sigma-convergence measures with conditional beta-convergence regressions, the methodological framework ensures that distributional convergence is not conflated with growth-based convergence. This distinction is particularly important in the post-crisis European environment, where income dispersion may decline even in the absence of strong catch-up mechanisms.

5. Results

5.1 Sigma-Convergence

The first part of the empirical analysis examines whether cross-country income dispersion within the European Union declined over the period 2010–2019. Sigma-convergence is assessed by estimating a linear time trend in the cross-sectional standard deviation of log real GDP per capita.

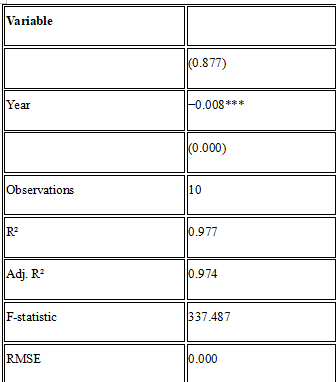

The results are reported in Table 1.

The coefficient on the time variable is negative and highly statistically significant (−0.008, p < 0.001), indicating a steady annual decline in income dispersion. The model explains a very large share of the variation in dispersion over time (R² = 0.977), suggesting that the downward trend is systematic rather than driven by isolated fluctuations.

This finding provides strong evidence of sigma-convergence across EU member states during the post-crisis decade. Income disparities narrowed consistently between 2010 and 2019. However, dispersion-based measures do not identify the underlying mechanism driving this process. To determine whether lower-income economies systematically grew faster than higher-income ones, conditional beta-convergence is examined next.

Table 1. Sigma-Convergence Trend (2010–2019)

Notes: Dependent variable is the cross-sectional standard deviation of log real GDP per capita. Standard errors in parentheses. *** p < 0.001.

5.2 Conditional Beta-Convergence

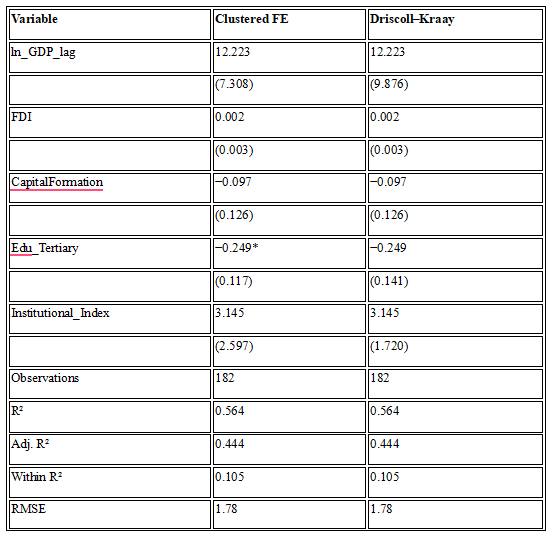

To investigate whether dispersion decline reflects systematic catch-up dynamics, conditional beta-convergence is estimated using a two-way fixed-effects panel model. Country and year fixed effects are included to control for time-invariant heterogeneity and common macroeconomic shocks.

Table 2 reports the results using clustered standard errors and Driscoll–Kraay standard errors.

The coefficient on lagged income (ln_GDP_lag) is positive (12.223) and statistically insignificant in both specifications. This result provides no evidence of conditional beta-convergence during the period 2010–2019. Lower-income EU member states did not grow systematically faster than higher-income economies once structural controls are included.

Among the controls, tertiary education shows a weak negative association with growth in the clustered specification (significant at the 10 percent level), although this effect becomes insignificant when using Driscoll–Kraay standard errors. Foreign direct investment, capital formation, and institutional quality do not display statistically significant effects in the short-run growth framework.

The within R² (0.105) indicates that the model explains a modest share of the within-country variation in growth rates, which is consistent with short-horizon macro panel analyses.

Taken together, the beta-convergence results contrast with the sigma-convergence findings. While income dispersion declined during the decade, this process does not appear to have been driven by a classical neoclassical catch-up mechanism.

Table 2. Conditional Beta-Convergence (2010–2019)

Notes: Dependent variable is real GDP per capita growth. Standard errors in parentheses. Clustered FE reports country-clustered standard errors. Driscoll–Kraay corrects for cross-sectional dependence. + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001.

6. Discussion

The empirical findings reveal an interesting divergence between dispersion-based and regression-based measures of convergence. While the sigma-convergence analysis indicates a clear and statistically significant decline in income dispersion across EU member states between 2010 and 2019 (Table 1), the panel regression results reported in Table 2 do not provide evidence of conditional beta-convergence. This combination of results suggests that the reduction in income inequality within the Union was not driven by a systematic catch-up mechanism in which poorer economies consistently grew faster than richer ones.

One possible explanation is that the post-crisis decade was characterized by broad-based recovery rather than asymmetric catch-up. Following the global financial crisis and the subsequent sovereign debt crisis, macroeconomic stabilization policies, monetary accommodation, and coordinated fiscal frameworks may have supported synchronized growth patterns across member states. Under such circumstances, income dispersion can decline even in the absence of a strong negative relationship between initial income and subsequent growth.

This interpretation is consistent with theoretical contributions emphasizing that convergence is not solely a function of initial income gaps, but also depends on structural and institutional alignment. If macroeconomic recovery is relatively uniform across countries, dispersion may narrow mechanically as extreme contractions are reversed, without implying a permanent shift in growth trajectories. The absence of a statistically significant beta coefficient in Table 2 therefore suggests that classical neoclassical convergence dynamics were not the dominant force during the observed period.

The weak and unstable effects of structural controls further reinforce this interpretation. Foreign direct investment and capital formation do not emerge as statistically significant growth drivers in the short-run panel framework. Tertiary education displays a weak negative association in one specification, but this result is not robust across alternative standard error corrections. Institutional quality, although theoretically central in long-run development frameworks, does not exert a statistically significant short-run effect within the fixed-effects model. These findings suggest that over a relatively short ten-year horizon, cyclical and policy-related factors may dominate structural determinants of growth.

The contrast between sigma- and beta-based results has been noted in previous convergence studies. Dispersion may decline due to common shocks, coordinated policy frameworks, or structural reforms affecting all countries simultaneously. In such settings, sigma-convergence can coexist with the absence of beta-convergence. The present results align with this perspective and indicate that the post-2010 period in the European Union may have been characterized more by stabilization and alignment than by classical income catch-up.

Importantly, these findings should not be interpreted as evidence against long-run convergence within Europe. Rather, they suggest that during the specific decade examined, convergence dynamics were subdued and potentially overshadowed by crisis recovery mechanisms and institutional stabilization. A longer time horizon or alternative identification strategies might reveal different dynamics.

From a policy perspective, the results imply that declining income disparities within the EU cannot be automatically attributed to structural catch-up processes. Sustainable convergence may require deeper structural reforms, productivity enhancements, and institutional strengthening rather than relying solely on cyclical recovery or macroeconomic coordination.

Overall, the evidence suggests that while dispersion in income levels narrowed during 2010–2019, the underlying mechanism was not a classical neoclassical convergence process. This distinction is crucial for interpreting post-crisis European growth patterns and for designing future cohesion and structural policies.

7. Conclusion

This study examined income convergence dynamics within the European Union over the period 2010–2019, focusing on the distinction between sigma-convergence and conditional beta-convergence. Using a panel dataset of 27 EU member states and applying two-way fixed-effects models alongside dispersion-based analysis, the paper provides evidence of declining cross-country income dispersion but finds no support for systematic catch-up growth.

The sigma-convergence results indicate a clear and statistically significant reduction in the cross-sectional standard deviation of real GDP per capita. Income disparities narrowed steadily throughout the decade. However, the conditional beta-convergence regressions do not reveal a negative and statistically significant relationship between initial income levels and subsequent growth rates. Lower-income member states did not grow systematically faster than higher-income economies once structural controls and fixed effects were included.

The coexistence of sigma-convergence and the absence of beta-convergence suggests that the observed reduction in income dispersion was not driven by classical neoclassical catch-up dynamics. Instead, the findings point toward a period characterized by macroeconomic stabilization, synchronized recovery following the global financial and sovereign debt crises, and relatively uniform growth patterns across member states.

The analysis also shows that key structural variables - such as foreign direct investment, capital formation, tertiary education, and institutional quality - do not exhibit robust short-run growth effects within the examined decade. This reinforces the interpretation that cyclical and policy-related factors may have dominated structural convergence mechanisms during the post-crisis period.

These results have several implications. First, declining dispersion should not be automatically interpreted as evidence of strong structural convergence. Second, sustainable long-run convergence may require deeper productivity-enhancing reforms and continued institutional strengthening rather than relying primarily on cyclical recovery dynamics. Finally, the findings highlight the importance of distinguishing between distributional convergence and growth-based convergence when evaluating cohesion policies within the European Union.

The relatively short time horizon represents a limitation of the present study. Future research could extend the analysis to longer periods, incorporate alternative identification strategies, or explore heterogeneity across regional subgroups within the EU. Nevertheless, the evidence presented here contributes to the broader debate on European convergence by clarifying the mechanisms underlying post-crisis income dynamics.

Reference

1.Acemoglu, D., Johnson, S., & Robinson, J. A. (2001). The Colonial Origins of Comparative Development: An Empirical Investigation. American Economic Review, 91(5), 1369–1401. https://doi.org/10.1257/aer.91.5.1369

2.Acemoglu, D., & Robinson, J. A. (2012). Why Nations Fail: The Origins of Power, Prosperity and Poverty. By Daron Acemoglu and James A. Robinson.

3.Anufrijev, A., Aničić, A., Dašić, G., & Tasić, S. (2026, January 27). ANALYSIS OF COMPETITIVENESS INDICATORS OF SMALL AND MEDIUM-SIZED ENTERPRISES IN THE WESTERN BALKANS REGION WITH SPECIAL REFERENCE TO THE FREQUENCY AND SHARE OF EMPLOYEES. Akcionarstvo. https://doi.org/10.65772/ak202514

4.Azariadis, C., & Drazen, A. (1990). Threshold Externalities in Economic Development. The Quarterly Journal of Economics, 105(2), 501–526. https://doi.org/10.2307/2937797

5.Barro, R. J., & Sala-i-Martin, X. (1992). Convergence. Journal of Political Economy, 100(2), 223–251.

6.Barro, R. J., & Sala-I-Martin, X. (1997). Technological Diffusion, Convergence, and Growth. Journal of Economic Growth, 2(1), 1–26. https://doi.org/https://doi.org/10.1023/A:1009746629269

7.Barro, R. J., & Sala-i-Martin, X. (2004). Economic growth (2nd ed). MIT Press.

8.Candida Bussoli & Ilenia Fraccalvier. (2025, August 19). Circular Economy Disclosure in European Banks: A Substantive Commitment or Symbolic Compliance? Društveni Horizonti. https://drustveni-horizonti.fdn.edu.rs/articles/60

9.Durlauf, S. N., & Johnson, P. A. (1995). Multiple regimes and cross-country growth behaviour. Journal of Applied Econometrics, 10(4), 365–384. https://doi.org/10.1002/jae.3950100404

10.European Commission. (2022). Cohesion in Europe towards 2050: 8th Cohesion Report. https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:52022DC0034&qid=1644393023846&from=EN

11.Fejes, Z. (2025, August 12). Evolution of Cross-Border Cooperation in the European Union – Challenges and Opportunities1. Društveni Horizonti. https://doi.org/10.5937/drushor2305055F

12.Islam, N. (1995). Growth Empirics: A Panel Data Approach*. The Quarterly Journal of Economics, 110(4), 1127–1170. https://doi.org/10.2307/2946651

13.Lalić, G., & Trifunović, D. (2026a). Economic and Institutional Convergence in Europe (2004–2023): EU Core, New Members, and the Western Balkans. Economies, 14(4), 142. https://doi.org/10.3390/economies14040142

14.Lalić, G., & Trifunović, D. (2026b). Income Convergence in Europe: The Role of Institutions and Structural Factors. Social Sciences, 15(3), 180. https://doi.org/10.3390/socsci15030180

15.Lalić, G., & Trifunović, D. (2026c). Institutional Quality as a Conditioning Factor of Convergence: Evidence from European Economies. World, 7(4), 51. https://doi.org/10.3390/world7040051

16.Lalić, G., & Trifunović, D. (2026d). Regulatory Volatility and Economic Growth in Europe: Heterogeneous Effects Across Institutional Development Stages. Sustainability, 18(5), 2658. https://doi.org/10.3390/su18052658

17.North, D. C. (1990). Institutions, Institutional Change and Economic Performance. Cambridge University Press. https://doi.org/10.1017/CBO9780511808678

18.Obućinski, D., Miljković, L., Ljubojević, N., & Krstić, S. (2025, November 26). THE ROLE OF MONETARY POLICY IN ENSURING MACROECONOMIC STABILITY. Oditor. https://doi.org/10.59864/Oditor42502SK

19.Phillips, P. C. B., & Sul, D. (2007). Transition Modeling and Econometric Convergence Tests. Econometrica, 75(6), 1771–1855. https://doi.org/10.1111/j.1468-0262.2007.00811.x

20.Phillips, P. C. B., & Sul, D. (2009). Economic transition and growth. Journal of Applied Econometrics, 24(7), 1153–1185. https://doi.org/10.1002/jae.1080

21.Rodrik, D., Subramanian, A., & Trebbi, F. (2004). Institutions Rule: The Primacy of Institutions Over Geography and Integration in Economic Development. Journal of Economic Growth, 9(2), 131–165. https://doi.org/10.1023/B:JOEG.0000031425.72248.85

22.Šare, D., Kosorić, D., & Tošev, D. (2026, January 19). THE IMPACT OF PUBLIC EXPENDIRURE AND PUBLIC DEBT ON ECONOMIC GROWTH DECLINE. Oditor. https://doi.org/Oditor%2082503DS

23.Anufrijev, A., Dašić, G., Aničić, A., & Tasić, S. (2025). Analiza pokazatelja konkurentnosti malih i srednjih preduzeća u regionu Zapadnog Balkana sa posebnim osvrtom na učestalost i udeo zaposlenih. Akcionarstvo, 31(1), 49–67. https://doi.org/10.65772/ak202514

24.Šare, D., Kosorić, D., & Tošev, D. (2026). The impact of public expenditure and public debt on economic growth decline. Oditor. https://doi.org/Oditor82503DS

Objavljeno u

God. 12 Br. 1 (2026)

Ključne reči

🛡️ Licenca i prava korišćenja

Ovaj rad je objavljen pod Creative Commons Attribution 4.0 International (CC BY 4.0).

Autori zadržavaju autorska prava nad svojim radom.

Dozvoljena je upotreba, distribucija i adaptacija rada, uključujući i u komercijalne svrhe, uz obavezno navođenje originalnog autora i izvora.

Zainteresovani za slična istraživanja?

Pregledaj sve članke i časopise