THE IMPACT OF TAX BURDEN LEVELS ON LONG-TERM ECONOMIC ACTIVITY

Abstract

This paper investigates the comparative long-term effects of tax burden levels on economic activity across developed and transitional European countries. The methodological approach is grounded in endogenous growth theory, which incorporates economic, social, and political variables to simulate the existence of a long-term relationship between tax policy and economic growth, with the aim of identifying recommendations for tax policy that support sustainable growth.

The assessment of the long-term relationship between tax burden levels and economic activity is conducted using annual data from balanced panel models covering 16 developed and 15 transitional European countries over the period 1995–2019. The analysis employs a dynamic panel model estimated via the Difference Generalized Method of Moments (GMM).

Empirical findings indicate that the impact of tax burden on long-term economic activity is nonlinear and statistically significant across both groups of countries. The results suggest that sustainable economic growth requires a reduction in tax burden levels.

Article

Introduction

Tax policy refers to a system of public policies aimed at generating state budget revenues through defining choices regarding the level of tax burden (the level of tax revenues) and the subject of taxation (the structure of tax revenues). By making decisions on the level and structure of tax revenues, the state directly influences the level of economic activity and the decisions of economic agents, thereby determining in the long run the values of basic macroeconomic aggregates on which the performance of the national economy is based. The extent to which tax policy affects economic growth, represented as a continuous process of improving the national economy’s ability to produce goods and services, is determined by the magnitude of the distortions created by taxes, which are manifested as a net loss of social welfare due to changes in relative prices and efficiency in the use of resources by the state.

The last two centuries of intensive development of nation-states have been marked by a continuous increase in the level of tax burden as a measure of social choice regarding the size and role of the modern nation-state, with simultaneous stable economic growth measured by the level of gross domestic product per capita. In the context of this fact, and the fact that tax revenues are the basis for the realization of state functions from its inception, the question arises about the role of tax policy in generating sustainable economic growth, that is, whether the economic growth of modern nation-states is due to the growth of total tax revenues (level of tax burden), or whether the achieved economic growth would have been greater if the tax burden had been lower or if the structure of tax revenues had been different.

Tax revenues represent a cost from the perspective of society, primarily caused by changes in relative prices due to taxation, that is, changes in the behavior of economic agents caused by changes in relative prices, and then by the efficiency with which the state uses collected tax revenues. However, the elimination of tax revenues, even as a theoretical concept, would have a far greater social cost compared to the reduction in social welfare – the cessation of the existence of the modern rule-of-law state, the disappearance of modern society, and the annulment of millennia of efforts aimed at building a civilization based on the rights and obligations of individuals and the state. Therefore, taxes are a necessity on which the modern state and modern society are based, and in the context of this fact and the state's efforts to maximize the level of social welfare, it is useful to determine the existence and nature of a possible long-term relationship between tax policy and economic growth, as one of the key segments of the social welfare function.

The subject of the research is a comparative analysis of the impact of tax policy on long-term economic growth in developed and transitional European countries, countries at different levels of economic, social, and political development (economic efficiency), through examining the impact of the first segment of tax policy, the level of tax burden, on the level of economic activity in the long run (level effect). The issue of the impact of the structure of tax policy on the dynamics of long-term economic growth (growth effect), as the second component of tax policy, represents a significantly broader concept that deserves to be analyzed separately. (Lalić & Trifunović, 2026)

Literature Review

The tax system represents a process by which the state transfers a portion of the income of taxpayers (businesses, households, and individuals) into the state treasury for the purpose of financing public policies. The introduction of taxes leads to changes in the relative prices of production factors, goods, and services, whereby taxes cause the reallocation of resources, changes in the structure of consumption and production, and the composition of gross domestic product. Changes in relative prices, as the main channel through which taxes affect economic activity and economic efficiency, occur through the introduction of taxes, as well as through changes in the level of tax burden and the structure of tax revenues (Brunner and Meltzer, 1969; Sarel, 1995).

The introduction or increase of taxes places taxpayers in a worse position for two reasons: first, taxation reduces disposable income; second, taxation makes certain production factors, goods, or services more expensive in comparison to others, which leads taxpayers to substitute the consumption of those factors, goods, or services with others. Through changes in relative prices, the tax system creates distortions in economic decisions, whereby taxes create excess burden or a welfare loss that exceeds the value of the taxes collected. Taxation causes market distortions by creating a tax wedge between production costs and the prices of goods and services, thereby disrupting the fundamental principle of economic efficiency that the marginal benefit of a good or service must be equal to the marginal cost of its production. In this way, taxes create welfare losses both for consumers and for producers (Rosen and Gayer, 2009; Burda and Wyplosz, 2012).

The second channel through which tax policy affects economic growth is a consequence of changes in the relative prices of production factors, final products, services, and other activities of taxpayers, and involves distortions in the decisions of economic agents caused by the introduction of taxes. The consequences of these distortions are manifested through the income effect of taxes (lower consumption of goods and services) and the substitution effect, which represents the extent to which the consumption of the taxed good or service decreases due to an increase in its relative price. In the process of transferring part of the income of taxpayers to the state, the tax system causes changes in the real disposable income of taxpayers, which leads to their reaction to the reduced income by adjusting decisions related to work, education, training, saving, investment, risk-taking, and entrepreneurship, as well as decisions related to consumption. By altering the economic decisions of taxpayers, the tax system creates additional excess burden, that is, a new welfare loss based on the excess burden caused by distortions in choices induced by tax policy (Rosen and Gayer, 2009; Stiglitz, 2013).

The third channel through which tax policy affects economic growth arises from the efficiency with which the state uses collected tax revenues, or as a consequence of the achieved level of economic, social, and political development of the country. (Marjanović, 2025)When defining public policies, the state seeks to achieve a broad range of social objectives, and is not primarily motivated by the economic principles of resource allocation. The state reallocates national resources in a manner that is not inherent to economic agents, which creates a gap in the efficiency of using resources collected through the tax system by the state compared to the efficiency with which resources are used by the private sector. The allocation of funds by the state typically yields a lower rate of return compared to the rate of return that would be achieved by the private sector. By directing a significant portion of limited societal resources toward unproductive purposes (economic efficiency is not the primary goal of the state), the state creates distortions that can be considered opportunity costs of resource reallocation, that is, additional excess burden representing a pure loss in terms of the efficiency of the national economy (loss of social welfare). This excess burden is directly dependent on the efficiency of the state.

It should be noted that economic efficiency and the concept of economic growth based on it are not the most important goals of the state, and thus the issue of the impact of tax policy on long-term economic growth is often a matter of choosing between economic efficiency and the level of social welfare. The modern state aims to maximize the level of social welfare through the definition of appropriate public policies, while economic growth is only one component of the complex social welfare function. Certainly, the tax system is one of the most important determinants of the level of social welfare, considering that it provides social benefits that cannot be measured through basic economic calculations, which is how taxpayers usually perceive reality. By providing public goods and services, the state ensures the necessary conditions for the functioning of modern society. Therefore, the existence of economic efficiency costs of the tax system, manifested as excess burden or welfare loss, needs to be thoroughly examined in the effort to create a tax system that minimizes such costs. The tax system generates losses that can be rationalized through the process of improving the existing tax system. In order to produce public goods and services, the state must impose taxes and deal with distortions. However, this should be done in the least inefficient way possible (Burda and Wyplosz, 2012).

A significant number of studies in the economic literature investigate the impact of tax policy on long-term economic growth. Arnold (2008) analyzes the impact of tax structure and the level of tax burden on economic growth using a sample of 21 OECD member countries over the period 1971 to 2004, and concludes that the total tax burden has a negative and statistically significant impact on long-term growth. Xing (2011) examines the impact of tax structure and the level of tax burden on long-term economic growth in a sample of 17 OECD countries from 1970 to 2004, and finds that the overall tax burden has a negative and statistically significant effect on long-term growth. Acosta-Ormachea and Yoo (2012) observe the impact of tax policy on long-term economic growth in the context of the country's level of development. Their sample includes 69 countries from 1970 to 2009, with data for 21 highly developed countries, 23 middle-income countries, and 25 low-income countries. For the entire sample, the tax burden exerts a negative and statistically significant effect. This study highlights one of the most important dimensions of the impact of tax policy on economic growth, which is the level of development of the country, from which its efficiency in designing public policies and managing limited national resources arises. McNabb and Le May-Boucher (2014) analyze the impact of tax policy on long-term economic growth using a sample of 110 countries from 1980 to 2010 (41 developed countries, 36 middle-income countries, and 33 low-income countries). Noting the much lower share of total tax revenues in GDP in low-income countries due to the large informal economy, tax evasion, and low tax morale, the authors emphasize the importance of efficient, strong, and developed institutions as a basic precondition for sustainable economic growth. The results show that in both developed and middle-income countries, the total tax burden has a positive but statistically insignificant effect on long-term growth, while in low-income countries, the impact is negative and also statistically insignificant. Esen and Aydin (2019) explore the optimal level of tax burden using a sample of 11 transitional countries from Southeast Europe and the Baltics, based on data from 1995 to 2014, and confirm the existence of a nonlinear effect of tax burden on long-term growth. The optimal level of tax revenues that maximizes growth is estimated at 18 percent of GDP for the entire sample, 18.5 percent for developing countries in the sample, and 23 percent for developed countries. Tax revenues exceeding the estimated threshold negatively affect long-term economic growth, while revenues below the defined threshold have a positive impact on growth. (McNabb & Le May-Boucher, 2014; Anufrijev et al., 2025)

There is also a considerable number of empirical studies that reject the existence of a long-term impact of tax policy on economic growth. Padda and Akram (2009) analyze the impact of tax policy on economic growth in a sample of seven transitional Asian countries from 1971 to 2007, concluding that tax policy has a temporary, transitional effect on long-term growth. Bakija and Narasimhan (2015) examine the effects of the level and structure of tax revenues on long-term economic growth in a sample of 79 countries from 1980 to 2010 and conclude that tax policy does not affect the level or growth rate of gross domestic product. Gbato (2017) analyzes the impact of taxation on economic growth in 32 Sub-Saharan African countries from 1980 to 2010, and concludes that the level of tax burden and the structure of tax revenues have no impact on long-term growth. The author points to the weak administrative capacity of the region and poorly designed tax systems in which most of the tax burden falls on the poorest segments of the population, along with discrimination against the poor in income distribution. Alinaghi and Reed (2018) examine the impact of tax policy and government expenditures on economic growth in a sample of 34 OECD countries from 1961 to 2010, and conclude that without taking into account other components of fiscal policy, tax policy does not have a significant long-term effect on economic growth.

Tax policy cannot be observed in isolation from other factors of economic, social, and political reality, nor from other components of the social welfare function (Lalić & Trifunović, 2026). Tax policy is only one segment of social reality, and its effects depend on the nature of societal relations, cultural patterns, the quality of the institutional framework, the political environment, the efficiency of the state, and other characteristics related to the level of economic, social and political development achieved. (Trifunović et al., 2024).

Methodology

The assessment of the long-term relationship between the level of tax burden (tax revenue level) and the level of economic activity is conducted using annual data from balanced panel models for a group of 16 developed and a group of 15 transitional European countries for the period from 1995 to 2019, through the estimation of coefficients with regressors in a dynamic panel model using the Difference Generalized Method of Moments.

The aim is to identify the strength and nature of the long-term relationship between the level of tax burden and the level of gross domestic product as an indicator of the level of economic activity or the country’s economic development. Based on the fact that the characteristics and effects of tax policy on economic activity depend on the achieved level of economic, social and political development of the country, the goal is also a comparative analysis of the impact of tax policy on the level of economic activity in two groups of countries, which differ in their level of development (economic efficiency)..

The dynamic form of the panel model is obtained by extending the static form of the model with the lag of the dependent variable, yi,t-1, which becomes a new variable in the set of explanatory variables of the model. The dynamic form of the panel model can thus be presented as follows:

![]()

In the basic specification of the dynamic panel model, yit represents the value of the dependent variable for the i-th observation unit in time period t; ψ is a scalar that indicates the importance of the adjustment dynamics of the dependent variable over time (importance of history, new informations), with |ψ|<1; yi,t-1 represents the first lag of the dependent variable; β1it is the intercept term that varies across both dimensions and captures differences between observation units and over time (heterogeneity of the model); к denotes the number of explanatory variables (regressors), while Xkit represents the value of the к-th explanatory variable for the i-th observation unit in time period t; βkit are the unknown regression parameters (slope coefficients) to be estimated, which show the impact of a one-unit change in the given regressor on the movement of the dependent variable, and which vary across observation units and over time; uit is the random error term with zero mean and constant variance, capturing the influence of unobserved factors that change over time and affect the dependent variable (Baltagi, 2008; Jovičić and Dragutinović Mitrović, 2011; Wooldridge, 2012).

By introducing the lag of the dependent variable into the set of explanatory variables, we introduce dynamics into the model by providing new information on the history of the dependent variable, which carries information on the impact of all variables that have historically shaped the dynamics of the dependent variable. This ensures more accurate parameter estimates compared to those obtained using methods designed for estimating the static form of the panel model (Greene, 2002; Roodman, 2009). It is a fact that the current level of gross domestic product is not determined solely by the regressors included in the model, but also by growth achieved in the previous period through the influence of factors not included in the model. Therefore, including the lag of the dependent variable as an additional regressor is especially important for obtaining valid estimates of the equation modeling the relationship between the level of tax burden and the level of gross domestic product as an indicator of economic activity.

An additional reason for estimating the dynamic form of the panel model lies in the fact that, when macroeconomic variables are the subject of the panel model, there is a pronounced simultaneity between economic growth (level of economic activity) and the model regressors, which is the main source of endogeneity in panel models (Bleaney, Gemmell, and Kneller, 2001). In the presence of endogenous regressors, which is inherent to modern macroeconomic conditions, the coefficient estimates obtained using the ordinary least squares method are biased and inconsistent. Therefore, it is necessary to control for the negative impact of endogenous regressors, which is enabled by the dynamic form of the panel model (Bleaney, Gemmell, and Kneller, 2001; Arnold, Bassanini, and Scarpetta, 2007; Elitza, 2007; Dackehag and Hansson, 2012).

The dynamic panel model used to estimate the long-term relationship between the level of tax burden and the level of economic activity in developed and transitional European countries, using the Difference Generalized Method of Moments, has the following form:

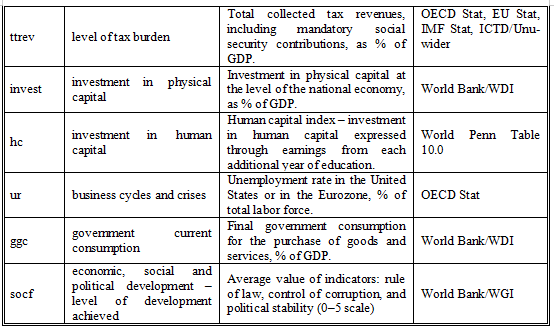

where lngdppci,t represents gross domestic product per capita as a measure of economic activity (economic development), expressed in US dollars at constant 2010 prices, the dependent variable (source: World Bank, World Development Index); lngdppci,t-1 is the first lag of the dependent variable; ψ is a scalar indicating the importance of the adjustment dynamics of the dependent variable over time; ttrevi,t represents the level of tax burden as the variable of interest, i.e. the amount of total tax revenues including mandatory social security contributions, expressed as a percentage of gross domestic product (source: OECD Stat, EU Stat, IMF Stat, ICTD/Unu-Wider); α0 represents the coefficient that captures the impact of the variable of interest on the dependent variable. The set of control variables, Xkit, is defined in accordance with the main assumptions of endogenous growth theory, aiming to include the fundamental factors of economic growth, i.e. the impact of investment in physical and human capital, economic cycles, government spending, and the achieved level of economic, social and political development of the country. The control variables include: investment in physical capital (infrastructure, factories, machinery and equipment) as a percentage of GDP, investi,t (source: World Bank, WDI); investment in human capital expressed as an index based on years of schooling and the earnings increase from each additional year of education, hci,t (source: Penn World Table, Version 10.0); unemployment rate (total unemployment rate) as a percentage of total labor force, representing the impact of economic cycles and crises on national economy. For developed countries, this is proxied by the unemployment rate of the United States, and for transitional countries by the unemployment rate of the Eurozone of 19 developed countries, uri,t (source: OECD Stat); government current consumption, defined as final consumption expenditure of the government for the purchase of goods and services, excluding investment and transfers, expressed as a percentage of GDP, ggci,t (source: World Bank, WDI); social factors as an indicator of the achieved level of social and political development of the country (indirectly, also of the level of economic development), expressed as the average value of three indicators: rule of law, control of corruption, and political stability, denoted socf, ranging from 0 to 5 (higher value indicates higher development level) (source: World Bank, World Governance Indicators). This variable encompasses the social and political factors of economic growth.

Table 1. Overview of variables and data sources

All model variables are expressed in annual data for the period from 1995 to 2019, covering two groups of countries defined by their level of economic, social and political development, as well as by the conditions under which they built and developed society and the national economy. Considering the significant differences in GDP per capita among the panel members, the dependent variable gdppc is expressed in natural logarithm in both country groups.

The group of developed European countries includes 16 countries: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Netherlands, Norway, Spain, Sweden, Switzerland, the United Kingdom and Portugal.

The group of transitional European countries includes 15 countries: Bulgaria, Estonia, Croatia, Hungary, Lithuania, Latvia, Romania, Russian Federation, Poland, Slovakia, Slovenia, Turkey, Czech Republic, Moldova and Ukraine.

Economic theory is based on the position that the tax burden has a positive impact on the level of economic activity in the long term, up to a certain level of total tax burden, regardless of the achieved level of development of the country, bearing in mind that by financing basic functions, the state creates conditions for the functioning of the national economy. So, a certain level of tax burden is necessary for the functioning of society, but in addition to the question of the structure of tax revenues, the essential question of the impact of tax policy on long-term economic growth is the level of tax burden that will not endanger long-term economic growth, that is, what is the level of tax burden at which the positive impact of taxes on the level of economic activity stops?

Considering the fact that countries with lower levels of economic, social and political development have a less efficient state, the assumption is that the positive impact of the level of tax burden on the level of economic activity stops being effective at a lower level of tax burden in countries with a lower level of development or economic efficiency. In order to confirm the validity of this theoretical assumption, it is necessary to econometrically determine the level of tax burden at which the positive effect of the total tax burden on the level of economic activity stops being effective in the group of developed and the group of transitional European countries, that is, the threshold of total tax burden (threshold effect).

The econometric method of determining the threshold of the impact of tax burden on the level of economic activity aims to establish the nature of the long-term relationship between the total tax burden and the level of gross domestic product, that is, to answer the question of whether there is a statistically significant level of tax burden at which the total tax burden changes the direction of its impact on gross domestic product (threshold of impact), and whether that level of tax burden differs for countries at different levels of economic, social and political development.

In order to determine the existence, level, and significance of the threshold of the impact of tax burden on the level of economic activity, a dynamic panel model with a threshold effect will be formulated in the following form (Hansen, 1999; Kremer, Bick, Nautz, 2009; Seo, Shin, 2016):

The level of tax burden, ttrevi,t, is both the threshold variable and the regressor of interest in the dynamic panel model: β1 and β2 presents the marginal impact effect of tax burden on GDP per capita level below and above the estimated threshold value γ. In practice, β1 and β2 represent coefficients for two different regimes of their interdependence. Variable Zi,t is a vector of exogenous and endogenous regressors (control variables), including the first lag of the dependent variable, lngdppci,t-1.

The assessment of the threshold effect of the level of tax burden on the level of economic activity will be conducted using the Seo-Shin test of dynamic threshold effect, which is designed for application to dynamic panel models characterized by threshold effects and endogeneity of regressors (Seo, Shin, 2016), whereby the hypotheses are defined as follows:

H0: β1=β2, there is no threshold effect, γ is not identified – the effect of the level of tax burden on the level of gross domestic product is represented by a linear function;

H1: β1≠β2, there is a threshold effect, γ is identified and statistically significant – the effect of the level of tax burden on the level of gross domestic product is represented by a nonlinear function.

Research results

The results of estimating the dynamic form of the panel model used to simulate the impact of the level of tax burden on the level of economic activity in the long term, along with additional test statistics for verifying the assumptions of the dynamic panel model, are presented in Table 2.

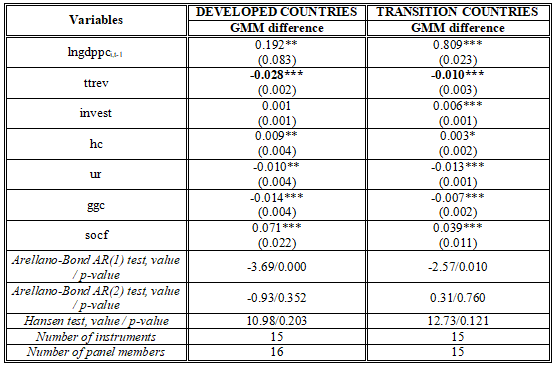

Table 2. Estimates of the dynamic panel model, dependent variable lngdppc

Note: Standard errors are shown in parentheses; ***, **, and * indicate significance levels of 1%, 5%, and 10%, respectively.

The level of tax burden has a negative and statistically significant effect on the level of economic activity in the long term in both groups of observed European countries. An increase in the tax burden, expressed as a percentage of gross domestic product, leads to a reduction in the level of economic activity in the long term (economic development), regardless of the country's achieved level of economic, social and political development.

The negative effect of the level of tax burden on the level of economic activity is stronger in the group of developed European countries, where an increase of 1% in the tax burden leads to a 2.8% decrease in economic activity, while in the group of transitional countries, the same increase leads to a 1% decrease. The dependent variable in the group of developed countries, as well as the variable of interest (tax burden), are stationary in the first difference and were included in the model as such, while in the transitional group, both the dependent variable and the variable of interest are stationary at level and were included accordingly. The values of the estimated coefficients for tax burden were obtained considering that the dependent variable is expressed in natural logarithm, unlike the regressors. Therefore, the estimated impact of tax burden on the movement of GDP per capita is calculated as follows:

(eestimated coefficient – 1) х 100 (4)

The control variables in the model have statistically significant effects in the expected theoretical direction. Investment in physical capital is not statistically significant in the group of developed European countries, which is expected due to the convergence effect and the fact that developed countries base their economic growth on the quality of human capital, investment in human capital, total factor productivity, and the quality of the social environment, with continuous improvement in indicators of social development, following decades of investment in physical capital. Investment in human capital has a positive and statistically significant effect on the level of economic activity in the long term in both groups of countries, while economic cycles, crises, and external shocks reflected through the unemployment rate, as well as government current consumption, have a negative and statistically significant effect regardless of the level of economic, social and political development of the country. The achieved level of social development has a positive and statistically significant effect in both groups of countries.

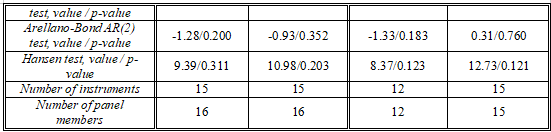

The realized values of test statistics and the corresponding p-values used to assess the quality of the defined dynamic panel model show that all assumptions of the model are satisfied. These include the absence of autocorrelation in the error term at the second lag, the adequacy of the selected set of instrumental variables for addressing endogeneity, and the acceptable number of instruments relative to the number of panel members, which is a necessary condition for obtaining valid and consistent estimates in the dynamic panel model.

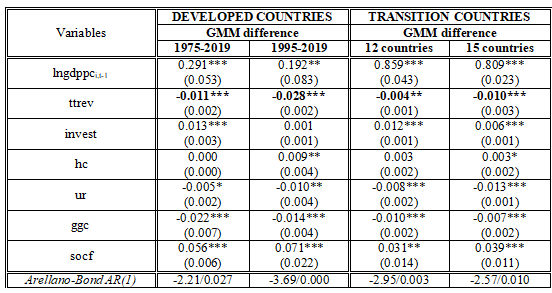

To test the robustness of the model’s parameter estimates, its specification and the selected determinants, we are re-estimated models using modified samples for both groups of countries, in accordance with available data. The sample for developed European countries was extended to cover the period from 1975 to 2019, since a broader database exists for this group. The sample for transitional countries was reduced by three countries, with the observed time period unchanged. The countries excluded from the transitional group are the Czech Republic, Slovakia, and Slovenia, for the following reasons:

- Although these countries underwent a transition process during the observed period, based on GDP levels they belong to the group of developed European countries;

- According to their level of economic, social and political development, these countries belong to the group of developed European countries, especially in terms of institutional development.

The results of the robustness check of the dynamic panel model estimates are presented in Table 3.

Table 3. Robustness check of the dynamic panel model, dependent variable: lngdppc

Note: Standard errors are given in parentheses; ***, **, and * denote significance levels of 1%, 5%, and 10%, respectively.

After testing the robustness of the parameter estimates in the dynamic panel model, the conclusion remains unchanged: an increase in the level of tax burden leads to a decrease in the level of economic activity in the long term, regardless of the achieved level of economic, social and political development. The statistical significance of the estimated coefficients for the regressors in the dynamic panel model, as well as the direction of causality, remains almost identical even after changing the sample in both groups of countries, indicating a high level of robustness of the defined model and the selected regressors for long-term economic activity dynamics.

To assess the nature of the effect of the level of tax burden on the dynamics of economic activity in the long term (whether the relationship is linear or nonlinear), considering that economic theory holds that tax burden has a positive effect on economic activity up to a certain level of total tax burden regardless of a country’s level of development—because the financing of basic state functions creates the conditions for the functioning of the national economy—a dynamic panel model with a threshold effect was also estimated.

The result of applying the Seo-Shin test for the dynamic threshold effect on the panel model defined by Equation (3) is shown in Table 4.

Table 4. Threshold effect of tax burden level on GDP, threshold variable ttrev

The existence of a statistically significant threshold effect of the level of tax burden on the level of economic activity indicates the nonlinear nature of the long-term relationship between tax burden and economic activity. Tax burden has a positive effect on the level of economic activity in the long term up to a certain level of burden, regardless of the country's development level. However, the positive effect of tax burden on economic activity ceases to take effect at a lower tax burden level in countries with lower development.

The threshold value for the level of tax burden in the group of developed European countries is 31.54% of gross domestic product, while in the group of transitional European countries it is 27.60%. The average tax burden in both groups of countries is significantly higher than the estimated threshold value (37.48% for the group of developed countries and 31.43% for the group of transitional countries). Therefore, the impact of tax burden on the level of economic activity in the long term is negative and statistically significant in both groups of countries.

Conclusion

The level of tax burden has a negative, statistically significant impact on the level of economic activity, which is represented by the level of gross domestic product per capita. An increase in the level of tax burden leads to a decrease in the level of economic activity in the long run, regardless of the achieved level of economic, social and political development of the country. The negative impact of the level of tax burden on the level of economic activity is stronger in developed European countries, where a 1% increase in the level of tax burden leads to a decrease in gross domestic product per capita by 2.8%, while a 1% increase in the level of tax burden in the group of transitional European countries leads to a decrease in the level of economic activity by 1%. The long-term relationship between the level of tax burden and the level of economic activity represents a nonlinear function of concave form, which means that the level of tax burden has a positive impact on the level of economic activity in the long run up to a certain level of tax burden, regardless of the achieved level of development of the country.

The positive impact of the level of tax burden on the level of economic activity in the long run ceases to be effective at a lower level of tax burden in countries at a lower level of development, as a result of a less efficient state, weak institutional framework, low level of tax morale and quality of tax administration, and a cultural, historical, political, and value framework that is tolerant of tax evasion. The threshold level of tax burden for the group of developed European countries is 31.54% of gross domestic product, while for the group of transitional European countries it is 27.60% of gross domestic product. The average tax burden for both groups of countries in the observed period is significantly higher than the established threshold and amounts to 37.48% for the group of developed European countries and 31.43% for the group of transitional European countries, so the impact of the level of tax burden on the level of economic activity in the long run is negative and statistically significant in both groups of observed European countries.

References

2.Alinaghi, N., & Reed, W.R. „Taxes and Economic Growth in OECD Countries: A Meta-Analysis“, University of Canterbury, Working Papers in Economics 18/09. (2018): 1-62.

3.Anufrijev, A., Dašić, G., Aničić, A., & Tasić, S. (2025). Analiza pokazatelja konkurentnosti malih i srednjih preduzeća u regionu Zapadnog Balkana sa posebnim osvrtom na učestalost i udeo zaposlenih. Akcionarstvo, 31(1), 49–67. https://doi.org/10.65772/ak202514

4.Arnold, J. „Do Tax Structures Affect Aggregate Economic Growth? Empirical Evidence from a Panel of OECD Countires“, OECD Economics Department Working Papers No. 643. (2008): 1-29.

5.Arnold, J., Bassanini, A., & Scarpetta, S. „Solow or Lucas? Testing Growth Models Using Panel Data from OECD Countries“, OECD Economics Department Working Papers No. 592. (2007): 1-28.

6.Bakija, J., & Narasimhan, T. „Effects of the Level and Structure of Taxes on Long-Run Economic Growth: What We Can Learn from Panel Time-Series Techniques?“ (Annual Conference of Taxation and Minutes of the Annual Meeting of the National Tax Association, 108 Annual Conference of Taxation, Boston, Sjedinjene Američke Države, 19-21. novembar, 2015).

7.Baltagi, B.H., Econometric Analysis of Panel Data (Chichester, West Sussex: John Wiley & Sons, Ltd, 1995).

8.Bleaney, M., Gemmell, N., & Kneller, R. „Testing the endogenous growth model: public expenditure, taxation and growth over the long run“, Canadian Journaal of Economics 34(1) (2001): 36-57.

9.Brunner, K., & Meltzer, A.H., „Relative Prices and Tax Policies: Some Preliminary Implications and Results“, Carnegie Mellon Universitu, Journal contribution (1969). https://doi.org/10.1184/R1/6707720.v1. (preuzeto 24.05.2015).

10.Burda, M.C., & Wyplosz, C., Makroekonomija. Evropski udžbenik 5. Izdanje (Beograd: Ekonomski fakultet Univerzieta u Beogradu, 2012).

11.Dackehag, M., & Hansson, Å., „Taxation of Income and Economic Growth: An Empirical Amalysis of 25 Rich OECD Countries“, Lund University, Department of Economics, Working Papers No. 2012:6 (2012): 1-32.

12.Elitza, M., „Using Arellano-Bond Dynamic Panel GMM Estimators in Stata. Tutorial with Examples using Stata 9.0 (xtabond and xtabond2)“. (2007). http://academia.edu/7518283/Elitz_Using_Arellano_ Bond_GMM Estimators. (preuzeto 17.07.2019).

13.Esen, O., & Aydin, C., „Optimal tax revenues and economic growth in transition economies: a threshold regression approach“, Global Business and Economics Review 21(2) (2019): 246-265.

14.Gbato, A, „Impact of Taxation on Growth in Sub-Saharian Africa: New Evidence Based on a New Data Set“, International Journal of Economics and Finance 9(11) (2017): 173-193.

15.Greene, W.H., Econometric Analysis 5th Edition (New Yersey: Prentice Hall, 2002).

16.Hansen, B.E., „Threshold effects in non-dynamic panels: Estimation, testing and inference“, Journal of Econometrics 93(2) (1999): 345-368.

17.Jovičić, M., & Mitrović Dragutinović, R., Ekonometrijski metodi i modeli (Beograd: Ekonomski fakultet Univerziteta u Beogradu, 2011).

18.Kremer, S., Bick, A., & Nautz, D., „Inflation and growth: New evidence from a dynamic panel threshold analysis“, SFB 649 Dicussion Paper No. 2009/036 (2009). http://hdl.handle.net/10419/39331 (preuzeto 12.12.2021).

19.Lalić, G., & Trifunović, D. (2026). Economic and Institutional Convergence in Europe (2004–2023): EU Core, New Members, and the Western Balkans. Economies, 14(4), 142, https://doi.org/10.3390/economies14040142

20.Lalić, G., & Trifunović, D. (2026). Institutional quality as a conditioning factor of convergence: Evidence from European economies. World, 7(4), 51. https://doi.org/10.3390/world7040051

21.Marjanović, T. (2025). ESG strategije u poslovanju trgovinskih lanaca sa osvrtom na dobavljače i potrošače. Društveni horizonti, 5(10), 105–127. https://drustveni-horizonti.fdn.edu.rs/sr/articles/69

22.Mc Nabb, K., & Le May-Boucher, P., „Tax Structures, Economic Growth and Development“, ICTD Working Paper No. 22 (2014). https://ssrn.com/abstract=2496470 (preuzeto: 18.03.2018).

23.Padda, I., & Akram, N., „The Impact of Tax Policies on Economic Growth: Evidence from South-Asian Economies“, The Pakistan Development Review 48(4) (2009): 961-971.

24.Roodman, D., „How to Do xtabond2: An Introduction to Difference and System GMM in Stata“, The Stata Journal 9 (2009): 86-136.

25.Rosen, H.S., & Gayer, T., Javne finansije 8. Izdanje (Beograd: Ekonomski fakultet Univerziteta u Beogradu, 2009).

26.Sarel, M., „Relative prices, Economic Growth and Tax Policy“, IMF Working Paper No. 95/113 (1995). https://ssrn.com/abstract=883259.

27.Seo, M.H., & Shin, Y., „Dynamic panels with threshold effect and endogeneity“, Journal of Econometrics 195(2) (2016): 169-186.

28.Stiglitz, J.E., Ekonomija javnog sektora 3. Izdanje (Beograd: Ekonomski fakultet Univerziteta u Beogradu, 2013).

29.Trifunović, D., Lalić, G., Deđanski, S., Nestorović, M., & Bevanda, V. (2024). Inovativni modeli i nove tehnologije u funkciji razvoja i kooperacije preduzeća i obrazovanja. Akcionarstvo, 30(1), 177–196. https://doi.org/10.65772/ak2024109

30.Wooldridge, J.M., Introductory Econometrics: A Modern Approach 5th Edition (Neshville: South Western College Publishing, 2012).

31.Xing, J., „Does tax structure affect economic growth? Empirical evidence from OECD countries“, Oxford University Centre for Business Taxation WP 11/20 (2011): 1-26.

Published in

Vol. 12 No. 1 (2026)

Keywords

🛡️ Licence and usage rights

This work is published under the Creative Commons Attribution 4.0 International (CC BY 4.0).

Authors retain copyright over their work.

Use, distribution, and adaptation of the work, including commercial use, is permitted with clear attribution to the original author and source.

Interested in Similar Research?

Browse All Articles and Journals