MAKROEKONOMSKE I BANKARSKO-SPECIFIČNE DETERMINANTE NETO KAMATNIH MARŽI: EMPIRIJSKI DOKAZI IZ SRBIJE

Apstrakt

U radu se analiziraju determinante neto kamatne marže (NKM) banaka u Srbiji u periodu 2007–2023. U analizi se koriste pokazatelji koji odražavaju stanje u bankarskom sektoru i odabrane makroekonomske varijable kao nezavisne varijable, dok se NKM posmatra kao zavisna varijabla. Primenom panel regresione analize identifikovane su ključne determinante koje utiču na neto kamatnu maržu banaka koje posluju u Republici Srbiji. Rezultati pokazuju da makroekonomski faktori imaju značajan uticaj na NKM. Referentna kamatna stopa ima pozitivan uticaj, dok devizni kurs ima negativan uticaj na NKM. Među varijablama bankarskog sektora, veličina banke i odnos kredita i depozita imaju statistički značajan negativan uticaj, dok Lernerov indeks, kao mera tržišne moći, ima pozitivan uticaj. Ostale analizirane varijable nisu statistički značajne.

Članak

Introduction

Net interest margin (NIM) is a widely used measure of bank profitability, defined as the ratio between net interest income and selected categories of assets reported in the balance sheet of an individual bank or the banking sector as a whole. When data availability is not a limitation, NIM can alternatively be expressed as the ratio of the aforementioned difference to interest-earning assets, which more accurately reflects the efficiency of the banking industry related to traditional credit-deposit intermediation. However, due to data constraints, research in practice more commonly defines NIM in relation to total assets.

Net interest margin indicates the efficiency of asset and liability management. Moreover, it serves as an indicator of the broader economic and regulatory situation in which banks operate. Understanding the factors that influence net interest margin is essential for decision makers, regulators and financial institutions themselves, especially in conditions of high interest rate volatility.

Determinants of NIM can be internal, which reflect banks’ operations, and external, which reflect the macroeconomic and institutional environment (Nuhiu et al., 2024; Kosumi & Zharku, 2024; Rossi et al., 2024). Despite the extensive literature on this topic, differences in identified determinants among countries and regions point to the need for deeper analyses that take into account the specific characteristics of national banking sectors. This paper examines the key factors that shape banks’ net interest margins in the Republic of Serbia, using panel regression analysis.

The domestic banking sector has had important structural changes in the past decades, including the process of transition, privatization and adaptation to the EU’s regulatory framework. Furthermore, due to the coordinated reaction to global economic disturbances, part of this period was also marked by unusually low interest rates. In such an environment, the analysis of factors affecting net interest margin gains additional importance. Special emphasis will be on the time span after the global financial crisis to analyze the resilience and adaptation of banks under conditions of reduced profitability, environmental change, and regulatory demands. Research results can help understand the margin structure in the Serbian institutional context and provide a basis for policies aimed at improving the banking system’s efficiency and stability. The paper includes three main parts. The first is a literature review on the determinants of net interest margin. This is followed by the data analysis, a detailed description of the methodology, and a discussion of results. The final section offers concluding considerations.

Literature review

The determinants of banks’ net interest margin have been the subject of numerous theoretical and empirical studies, given the importance of this indicator for assessing the profitability and efficiency of the banking sector. The basic theoretical model for analyzing the net interest margin was developed by Ho and Saunders (1981). This model (known as the dealership model) sees the bank as an intermediary between depositors and borrowers, attempting to avoid exposure to risk as much as possible. It is assumed that in choosing the structure of its loans and the sources of funding for those loans, the bank aims to insulate (isolate) itself from the effects of risk—this is known as the hedging hypothesis. The underlying assumption is that aligning the weighted average maturities of financial assets and liabilities allows banks to avoid potential reinvestment and refinancing risks that would otherwise result from differences in their respective maturity profiles. The risk identified by the model is the interest rate risk arising from changes in interest rates. Liquidity risk—which can be a practical consequence of maturity mismatches between assets and liabilities—is not specifically analyzed, as the model assumes that reinvestment and refinancing will always be available, albeit under suboptimal conditions. Thus, liquidity risk is essentially reduced to interest rate risk. To give the model a more elegant mathematical form, simplifications were necessary, and many of the risks that banks face in practice were abstracted from the model.

Net interest margin points to the bank’s operational efficiency and the impact of competition on two traditional banking markets: the deposit and loan markets. To a large extent, NIM is a parameter that the bank sets as its target when they want to cover all the risks and costs that arise in financial intermediation (Obeid, 2024). Banks pursue target efficiency by applying various business strategies. One way is to operate with the maximum possible spread between lending and deposit interest rates. Nonetheless, competition limits banks’ ability to increase operational efficiency in this way. Therefore, it can be concluded that NIM optimization is nothing more than the response of each individual bank to prevailing market conditions. The level of NIM is influenced by both interest rate policy and the structure of assets and liabilities available to the bank, with a mutual interdependence existing between these two factors.

Maintaining an adequate net interest margin is essential for generating income that allows banks to build up capital buffers in response to higher risk exposure. (Angbazo, 1997, p. 56). For that reason, in empirical research on net interest margins, various determinants pointing to the degree of risk exposure often appear as potentially statistically significant. These include, for example, credit risk (Wong, 1997; Angbazo, 1997), liquidity risk, the degree of financial leverage, operating costs, bank size, non-interest income, and others.

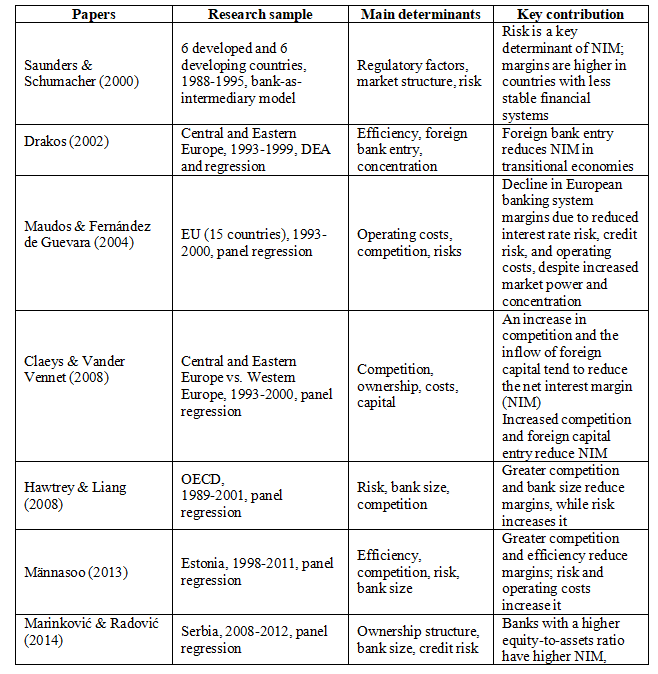

Banks set the margins taking into account the following factors: level of risk aversion and market competition, bank size and interest rate volatility. Many studies employ cross-country samples to explore whether common factors influence margin formation across different banking systems.Table (1) shows the studies relevant for this paper.

Table 1. Review of empirical studies

Empirical literature differs in geographical focus and methodological approach. However, most papers single out similar groups of determinants: selected features of the national banking system, macroeconomic and institutional determinants. So, the most commonly used are: bank size (larger banks often achieve lower margins due to economies of scale), efficiency (higher operational efficiency is associated with lower costs and higher margins), credit risk (higher risk requires a higher premium embedded in interest rates), and the structure of funding sources (banks that rely more on expensive sources of capital tend to have higher margins). Among macroeconomic and institutional variables, the most frequently cited determinants of NIM include: inflation (higher inflation often leads to higher margins due to a greater uncertainty premium), gross domestic product (higher economic activity usually contributes to lower margins as credit risk and unit service costs decrease), regulatory framework and the degree of financial liberalization (more restrictive regulation can increase operating costs and affect margins), and market structure, i.e., the level of competition (in oligopolistic structures, banks have the ability to set higher margins, while the presence of foreign banks can increase competition and reduce margins of domestic banks) (Ristić et al., 2023).

Recent studies have continued to explore the determinants of net interest margins in the context of prolonged low interest rate environments and structural changes in banking systems. For instance, Borio et al. (2017) and Claessens et al. (2018) emphasize the role of monetary policy conditions and bank business models in shaping interest margins. More recent research highlights the importance of market power, regulatory environment and macroeconomic volatility for margin formation in both developed and emerging banking systems.

Männasoo (2013) analyzes the determinants influencing the NIM of banks in Estonia from 1998 to 2011. The independent variables are: market structure, interest rate volatility, efficiency, liquidity, and credit risk. The research results confirmed that NIM is primarily determined by risk and the market structure of the banking sector. Bustos-Contell et al. (2019) conduct a study to identify the determinants of NIM for banks operating in Spain from 1985 to 2015. The analysis confirm that macroeconomic determinants have a more significant impact before the crisis, while industry-specific determinants are more influential after the crisis.

Among papers analyzing the determinants of net interest margin of banks operating in several countries, we single out research by Saunders & Schumacher (2000) who use a sample of 614 banks operating in six selected European countries and the USA from 1988 to 1995. The results show that regulatory factors, such as limits on deposit interest rates, required reserves and capital adequacy ratios, have a significant impact on NIM. Also, segmentation and restrictions within the banking system increase the existing banks’ monopoly power, leading to higher margins. Macroeconomic volatility of interest rates also significantly affects NIM, suggesting that policies aimed at reducing that volatility may reduce bank margins. Drakos (2002) examines the banking sector’s efficiency in Central and Eastern European countries during the transition period and analyzes the impact of foreign bank entry on net interest margins. The analysis covers 185 banks from transition countries, including Bulgaria, the Czech Republic, Hungary, Poland, Romania and Slovakia, in the period from 1993 to 1999. The results of the panel analysis show that foreign bank entry decreased NIM in the observed transition countries during the analyzed period.

Maudos & Fernández de Guevara (2004) examine the factors influencing net interest margins in major European Union banking markets over the period 1993–2000. They find that operating costs and risk levels played a significant role. Despite widespread mergers and acquisitions during this time, reductions in operational costs and lower interest and credit risks offset the potential increase in NIM, suggesting that market structure and competition alone could not fully explain changes in NIM.

Hawtrey and Liang (2008) examine the determinants of net interest margins across the banking sectors of fourteen OECD countries over the period 1987–2001. Their results indicate that both bank scale and managerial performance exert a significant negative influence on NIM, whereas factors such as market power, risk aversion, interest rate volatility, credit risk, the opportunity cost of holding liquid assets and implicit interest have a positive and significant effect. Managerial efficiency is defined as the ratio of operating expenses to gross income, where lower efficiency corresponds to narrower margins. Bank size is measured as the logarithm of total loan volume, where larger loan portfolios reduce unit costs due to economies of scale, ultimately resulting in narrower interest margins.

Kasman et al. (2010) conducted the analysis on a sample of selected countries from Central and Eastern Europe between 1995 and 2006. Their study compares banks in countries that recently joined the EU, such as Malta and Cyprus, with banks operating in candidate countries including Croatia, Macedonia, and Turkey. The authors intend to check the impact of consolidation of the banking sector, and thus distinguish two observation periods: the first, from 1995 to 2000, and the second, from 2001 to 2006. In the first analyzed period, most industry-specific and market variables confirm a positive impact on NIM. In the second period, the influence of macroeconomic variables diminished due to reduced disparities among the analyzed countries, which led to an increased importance of industry-specific variables. Among them, capital adequacy confirms its significance in old, but not new, EU members, while the concentration index emerges as an important determinant of NIM in both sets of countries, although the effect operated in opposite directions.

In the context of Serbia and the Western Balkans, research is still relatively limited. Marinković and Radović (2014) analyze the determinants of net interest margin in the Serbian banking sector. They use panel regression analysis to check the influence of the characteristic features of individual banks, the banking sector and macroeconomic determinants on NIM, in the context of different ownership structures and bank sizes. The results indicate that macroeconomic determinants do not have a significant effect on the margin when banks operating within the same economic and institutional environment are considered as statistical units. When it comes to industry-specific variables, the analysis confirms that banks with a higher equity-to-assets ratio record higher net interest margins. Regarding the impact of credit risk, their research points to the the opposite, i.e. negative relationship with NIM. Of industry-specific indicators, market concentration is a significant factor, with the expected direction of influence. Additional importance of this paper comes from the analysis of differences in NIM between banks of different sizes and ownership structures. The findings indicated that larger and foreign banks exhibit superior risk management efficiency. Plakalović and Alihodžić (2015) analyze the determinants of net interest margin of banks in Bosnia and Herzegovina from 2008 to 2013. Using a multiple linear regression model, the authors analyze the impact of macroeconomic and microeconomic determinants on NIM. Their findings confirm a negative relationship between macroeconomic determinants (gross domestic product growth and inflation) and net interest margin, while industry-specific variables (liquidity risk, credit risk and operating costs) confirm a positive relationship with NIM. Todorović et al. (2024) analyze the determinants of net interest margin in the banking sectors of Southeast Europe during the period from 2012 to 2021. Their results indicate that both the cost of capital in real terms and currency fluctuations, along with bank sector magnitude and degree of market concentration, are positively associated with NIM. In contrast, variables such as GDP, inflation, capitalization, liquidity and credit risk are found to have no statistically significant impact. In a somewhat different methodological framework, Marjanović et al. (2023) use DEA and the Tobit regression method in a similar period to look at banks in Serbia as statistical units, and find a negative impact of high market concentration of the banking sector, GDP and financial crisis, while inflation is a variable with a positive influence on bank efficiency.

Methodology and discussion

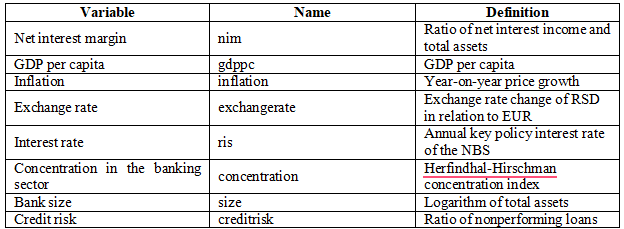

Given that the objective of this paper is to analyze the impact of the determinants of banks’ net interest margin in the Republic of Serbia from 2007 to 2023, we focus on selected industry-specific and macroeconomic indicators (Table 2).

Table 2. Description of key indicators

The Lerner index is used as a proxy for banks’ market power and reflects the ability of banks to set prices above their costs. Higher values of the index indicate greater market power and lower competitive pressure in the banking sector. In this study, the index is calculated using accounting data on banks’ total income and total expenses, as presented in Table 2, which represents a commonly applied approach in empirical banking research.

The research sample includes 20 banks (n=20): 3 Banka, Addiko banka, Adriatic banka, AIK, ALTA, API, Banca Intesa, Bank of China Srbija, Poštanska štedionica, Erste Bank, Eurobank Direktna, Halkbank, MIRABANK, NLB Komercijalna banka, OTP, ProCredit Bank, Raiffeisen Banka, Srpska Banka, Unicredit Bank and Yettel Bank in the period from 2007 to 2023 (t=17). The panel is not balanced, as some banks do not have data for the entire time span. Data were obtained from the National Bank of Serbia’s website. The following graph shows banks’ net interest margin trend in the observed period.

Diagram 1: NIM trend in the selected Serbian banks in the period 2007-2023

Source: NBS, authors, https://www.nbs.rs/sr_RS/finansijske-institucije/banke/bilans-stanja (accessed on 10 April 2025)

Note: 1-3 Banka, 2-Addiko banka, 3-Adriatic banka, 4-AIK, 5-ALTA, 6-API, 7-Banca Intesa, 8-Bank of China Srbija, 9-Poštanska štedionica, 10-Erste Bank, 11-Eurobank Direktna, 12-Halkbank, 13-MIRABANK, 14-NLB Komercijalna banka, 15-OTP, 16-ProCredit Bank, 17-Raiffeisen Banka, 18-Srpska Banka, 19-Unicredit Bank i 20-Yettel Bank

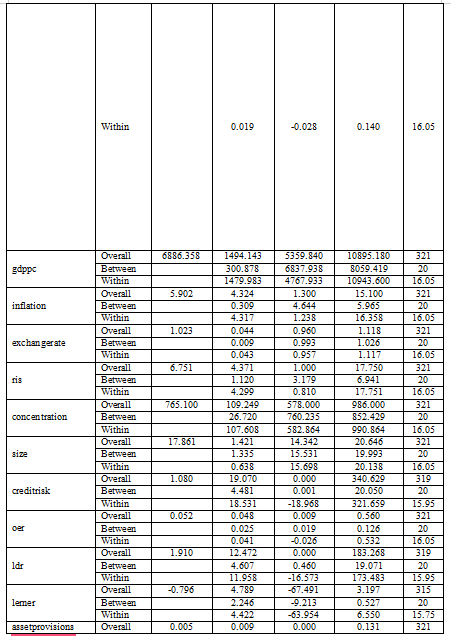

The data analysis was conducted using Stata 12. Table 3 presents the descriptive statistics of the variables.

Table 3. Data summary

![]()

![]()

Source: Authors

Certain variables exhibit relatively large ranges, particularly credit risk, loan-to-deposit ratio and the Lerner index. These extreme values may be attributed to differences in banks’ balance sheet structures, as well as to specific episodes during the observed period when some banks experienced unusually low profitability or temporary losses, which affected the calculated values of certain indicators.

With the aim of testing the impact of selected industry-specific and macroeconomic variables on NIM, we employ panel regression. The dependent variable is nim.

In our analysis, the Hausman test results (χ²(6) = 3.44, p = 0.752) fail to reject the null hypothesis, suggesting that the random-effects model is more suitable. The Breusch-Pagan LM test assesses whether there is no unit-specific variance, i.e. whether the simple OLS model adequately captures the data structure. The test outcome (χ²(1) = 715.28, p < 0.001) rejects the null hypothesis, confirming the presence of panel effects.

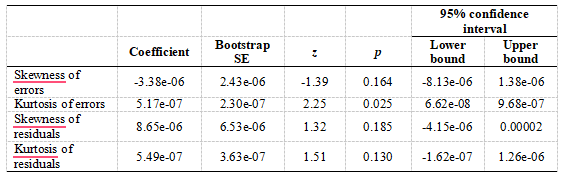

Model diagnostics involve several tests. The Fisher-type test indicates that GDP per capita (gdppc), inflation, exchange rate, concentration and size are non-stationary and therefore require first-order differencing. To assess residual normality, kurtosis and skewness tests for panel data are applied. The findings are summarized in Table 4.

Table 4. Test of normality of residuals

Source: Authors

Analysis of the distribution characteristics of errors and residuals shows that there are no statistically significant deviations from symmetry (p > 0.16 for all skewness estimates). However, the kurtosis coefficient of the error term is positive (coefficient = 5.17e-07) and statistically significant (p = 0.025), which indicates that distribution of errors is more peaked than the normal distribution. The kurtosis of residuals is not statistically significant (p = 0.130), which shows that the residuals approximately follow a normal distribution.

The Wooldridge test for autocorrelation indicates the presence of serial dependence in the panel observations (F(1, 19) = 10.294, p = 0.005). The Breusch-Pagan/Cook-Weisberg test detects heteroskedasticity in the dataset (χ²(20) = 9005.56, p < 0.001). To assess potential multicollinearity, variance inflation factors (VIF) and tolerance values are calculated. All independent variables exhibit VIF values below 10 and tolerance values above 0.1, indicating no serious multicollinearity. Finally, cross-sectional dependence among banks is examined using the Pesaran test. The null hypothesis about the absence of cross-sectional dependence is not accepted (CD = 4.622, p < 0.001), which indicates dependence among banks. Based on the conducted tests, we opt for a random-effects model, and due to the interdependence between banks, we use Driscoll-Kraay estimator to correct standard errors. The Driscoll–Kraay estimator is applied in order to obtain robust standard errors that are consistent in the presence of heteroskedasticity, serial correlation and cross-sectional dependence. Since the diagnostic tests indicate the existence of autocorrelation, heteroskedasticity and cross-sectional dependence among banks, the Driscoll–Kraay correction provides more reliable inference compared to conventional random-effects estimators. Table 5 shows the results of the analysis.

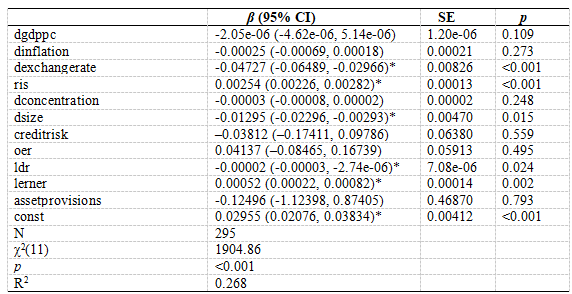

Table 5. Random-effects GLS regression with Driscoll–Kraay standard errors

*p < 0.05

Source: Authors

The regression equation is as follows:

nim = 0.02955-2.05*10-6*dgdppc-0.00025*dinflation - 0.04727*dexchangerate + 0.00254*ris - 0.00003*dconcentration - 0.01295*dsize – 0.03812*creditrisk + 0.04137*oer - 0.00002*ldr + 0.00052*lerner - 0.12496*assetprovisions

The model is significant (χ²(11) = 1904.86, p < 0.001). Together, the variables explain 26.8% of the variance in the dependent variable (R² = 0.268). Significant predictors of the dependent variable are: Exchange rate change (dexchangerate) (β = -0.04727, 95% CI = [-0.06489, -0.02966], p < 0.001); Key policy interest rate (ris) (β = 0.00254, 95% CI = [0.00226, 0.00282], p < 0.001); Change in bank size (dsize) (β = -0.01295, 95% CI = [-0.02296, -0.00293], p = 0.020); Loan-to-deposit ratio (ldr) (β = -0.00002, 95% CI = [-0.00003, -2.74e-06], p = 0.020) and Lerner Index (lerner) (β = 0.00052, 95% CI = [0.00022, 0.00082], p = 0.002).

It should be noted that several variables (GDP per capita, inflation, exchange rate, concentration and bank size) are included in the model in their first differences. Therefore, the coefficients of these variables reflect the effect of changes in these indicators on net interest margin rather than their absolute levels. The interpretations of the coefficients are as follows. A one-unit increase in the annual change of the exchange rate (dexchangerate) is associated with a decrease in net interest margin (NIM) of approximately 0.047, holding other variables constant. A one-percentage-point increase in the key policy interest rate (ris) is associated with an average increase in NIM of about 0.0025, ceteris paribus. A one-unit increase in the annual change of bank size (dsize) is associated with an average decline in NIM of approximately 0.0129, holding other factors constant. A one-unit increase in the loan-to-deposit ratio (ldr) is associated with a decrease in NIM of about 0.00002, other variables remaining unchanged. Finally, a one-unit increase in the Lerner index (lerner) is associated with an average increase in NIM of approximately 0.0005, holding other variables constant.

Conclusion

This study employs panel regression analysis to determine the main factors influencing the net interest margin (NIM) of Serbian banks during the analyzed period. The results confirm the significant impact of macroeconomic variables, i.e. key policy interest rate and exchange rate, on NIM. An increase in the key policy interest rate has a positive impact on net interest margin, which is in line with expectations: higher reference rates signal banks to increase lending interest rates, thereby increasing income from loan placement. On the other hand, the depreciation of the domestic currency (weakening of the dinar) negatively affects the margin, which may be a consequence of high borrowing costs and higher exchange rate risk in the banking sector.

Among banking sector characteristics, bank size is negatively correlated with net interest margin, suggesting that larger banks have lower margins, potentially due to more intense competition and lower reliance on interest income. The loan-to-deposit ratio (ldr) also demonstrates a negative effect, indicating that greater exposure to lending relative to collected deposits may contribute to a decline in the margin, either through increased funding costs or higher levels of risk. Lerner index has a significant and positive impact on the margin, which confirms that banks with greater market power, i.e. the ability to influence market prices, achieve higher net interest margins. Contrary to expectations, other analyzed variables, such as inflation, concentration index, credit risk, operational efficiency and asset provisions for asset losses (loan loss provisions), do not show a statistically significant impact on net interest margin in the analyzed sample.

The findings have several policy implications. Monetary authorities should be aware that changes in the policy rate and exchange-rate movements materially affect banking-sector margins. For bank managers, the results suggest that balance-sheet structure and market positioning remain important drivers of profitability.

This study is subject to several limitations. The analysis covers only Serbian banks and selected explanatory variables, while institutional quality, ownership structure and broader regulatory changes were not explicitly modeled. Future research may extend the sample to regional comparisons and dynamic panel techniques

Objavljeno u

God. 12 Br. 1 (2026)

Ključne reči

🛡️ Licenca i prava korišćenja

Ovaj rad je objavljen pod Creative Commons Attribution 4.0 International (CC BY 4.0).

Autori zadržavaju autorska prava nad svojim radom.

Dozvoljena je upotreba, distribucija i adaptacija rada, uključujući i u komercijalne svrhe, uz obavezno navođenje originalnog autora i izvora.

Zainteresovani za slična istraživanja?

Pregledaj sve članke i časopise