PERCEPCIJE ZAPOSLENIH U TRANSPORTNIM PREDUZEĆIMA O UPRAVLJANJU TROŠKOVIMA

Apstrakt

U savremenim poslovnim uslovima koje obeležavaju nacionalne i međunarodne ugovorne integracije i akvizicije, globalizacija ponude i potražnje za transportnim uslugama, izuzetno brz razvoj konkurencije usled pojave novih preduzeća iz zemalja koje tradicionalno nisu bile orijentisane ka međunarodnom transportu, kao i rast značaja naprednih softverskih alata, upravljanje troškovima dobija sve veću važnost. Menadžment transportnih preduzeća prepoznaje da se ključni mehanizam očuvanja konkurentske pozicije zasniva upravo na efikasnom upravljanju troškovima. Cilj ovog rada je da ispita percepcije zaposlenih u transportnim preduzećima u Srbiji u vezi sa upravljanjem troškovima. Rezultati istraživanja pokazuju da zaposleni prepoznaju značaj kontrole troškova, ali da nedostatak transparentnosti, obuke i međusektorske komunikacije ograničava njenu efikasnu primenu. Uočene su jasne razlike između menadžerskog i nemenadžerskog kadra, pri čemu menadžeri dosledno ostvaruju više skorove, što ukazuje da radna pozicija i blizina procesu odlučivanja značajno oblikuju percepcije o upravljanju troškovima.

Članak

Introduction

In a world of open borders, with predominantly globalized economies and reduced political and economic barriers to entering new foreign markets, companies have gained the opportunity to operate more successfully and achieve higher profit margins. An International Monetary Fund study (IMF, 2016) points out that this reflects the decline in effectively applied tariffs and non-tariff barriers burdening trade costs. Anderson and Wincoop (2004) note that transportation costs in global trade, representing the largest component of non-tariff costs, have been significantly reduced. Theorists (Davis & Drumm, 2002) who investigated transport costs as a share of total logistics costs observed that they had risen to as much as 44% in 2002. Thus, although transport costs in absolute terms have decreased, their share in logistics costs has increased. This is a growing number of scholars who are devoting attention to research in this area. Such a trend can be considered expected, given the structure of transport costs, their individual dependence on the movement of other input prices, and the fact that they are not set by political decision, but rather by economic principles. In interpreting this, it becomes clear why transport costs have not fallen as much or as rapidly as artificial barriers have been removed by political decision. This was noted by Amjadi and Yeats (1995), as well as other researchers (Radelet & Sachs, 1998), who observed that transport costs appear to be more persistent than non-tariff barriers eliminated by political decisions in the pursuit of trade liberalization.

“The transport sector plays a significant role in the functioning of the overall economy” (Miljković & Nikolić, 2024, p. 7). The same authors emphasize its importance from the supply perspective, noting that it primarily contributes by enabling market expansion, increasing production, and generating multiplier effects, while also influencing production and employment during the phases of infrastructure construction and operation. The World Trade Organization published a report highlighting that transport costs constitute the main non-tariff barrier, often proving to be a more effective form of protection than politically designed tariffs and non-tariff barriers (WTO, 2013). This has been empirically confirmed by various researchers studying countries in South America (Micco & Perez, 2002) and Asia (De, 2006). Theorists (Camison-Haba & Clemente-Almendros, 2020), analyzing the UN Conference on Trade and Development report (UNCTAD, 2015), emphasized their estimate that international transport costs accounted for 9% of a country’s import value, ranging from 6.8% in developed countries to 11.4% in developing countries during the 2005–2014 period.

Based on the objective of the research of this study, three research questions have been carefully formulated to provide a structured framework for investigating employees’ perceptions of cost management in transport companies:

· RQ1 - How does the level of employees' awareness of cost management affect their perception of the importance of cost control?

· RQ 2 - Is there a difference in attitudes towards cost management depending on the employees' job position?

· RQ3 - How do different aspects of organizational support (strategy, modern methods, motivation, rapid response and communication) affect the perception of cost management effectiveness in transport companies?

The efficiency of transport organizations is ensured by maximizing operational outcomes while simultaneously minimizing associated costs. Conceptually, the economic effect of transport can be defined as the net difference between the results of an organisation’s economic activities and the expenditure required to achieve them.

Specific features of costs in transport companies

Financial sustainability in businesses is shaped by a range of complex internal and external factors, among which the efficiency of cost management plays a critical role (Srebro et al., 2021; Milojević et al., 2024). Transport costs account for a significant share of companies’ total expenses, as an increasing quantity of goods, whether fast- or slow-moving consumer goods, are not produced in geographical proximity to the customer and actual consumption. Consequently, companies’ interest in examining these costs has grown over time. In the context of globalization of the world market, with the extension and increasing complexity of supply chains, transport costs have been recognized as a primary indicator of supply chain efficiency (Zeng & Rossetti, 2003). The expected reduction of transport costs in the global economy, resulting from the application of new engineering solutions both in transport vehicles and in improvements to transport infrastructure (Glaser & Kohlhase, 2004), has led to greater efficiency in goods distribution. This, in turn, enables better financial performance for companies—not only manufacturers, but also transport and trading firms—since all entities within this chain benefit from such technological progress. Manufacturers can increase production due to theoretically higher demand driven by lower prices; trading companies can increase profit margins by capturing part of the difference between old and new transport costs, while transport companies can also achieve higher profit margins by retaining part of the difference between previously higher and subsequently lower operating costs. Djankov, Freund, and Pham (2010), as well as Hummels (2007), note that in global trade, transport costs represent the most significant factor guiding foreign investment and entry into foreign markets.

Researchers (Kufel, 1990; Nowakowska-Grunt, 2013) emphasize that logistics costs constitute a specific category of costs, referring to the monetary value spent by a company in planning, implementing, and controlling non-technical processes of moving all forms of materials and goods through time and space. Other theorists (Stępień, Legowik-Świącik, Skibińska, & Turek, 2016) argue that logistics costs are a critical element of companies’ financial positions and cost structures. In this sense, they are recognized as a decisive factor for maintaining and strengthening a company’s competitive position in the market (Chow & Gill, 2011; Zamora & Pedraza, 2013), a view confirmed by Pešut (2009) in analyzing the report Global Supply Chains, Transport and Competitiveness by the United Nations Economic Commission for Europe.

The classification and structuring of logistics costs were addressed by Szałek (1994), while Pfohl (2022) focused on the complexity of costs associated with warehousing operations. Kwejt (1982), in his research, examined the structuring of logistics costs, paying particular attention to both strict transport costs and various costs of inventory management. He also considered shortages and penalties arising from supplier errors, a topic later presented at a textbook level by Skowron-Grabowska (2014).

The development of the concept of “smart logistics,” which incorporates highly promising principles such as Mobile Robotic Systems, Mobile Automated Platforms, and Multi-Agent Cloud, has been studied by researchers (Gregor, Krajčovič, & Wiecek, 2017). They elaborate on the notion of a “smart connected product” and present it within the context of smart logistics. These researchers identify current logistics solutions as environmentally risky, overly demanding for the workforce, and costly, estimating that by 2030, half of European factories will employ their own logistics solutions supported by autonomous mobile robotic systems. The digitization of transport and its impact on transport company costs has also been examined by Stalmašeková, Genzorová, Čorejová, and Gašperová (2017), who highlight the significance of information and communication technologies for the transport industry.

Dan (2022) investigates problems in logistics and develops countermeasures for challenges encountered by companies in managing transport costs. He underscores the role of transport costs within logistics and dissects their composition. In interpreting the current state of the industry, he observes a serious brain drain, inadequate management of transport costs, and a clear need for improving the quality of transport. As a goal for researchers, he proposes the development of a market- oriented transport system that will be more cost-efficient and more competitive in the market.

Challenges in managing transport costs in a dynamic environment

The limitation of resources imposes upon companies the requirement of adequate cost management to increase business efficiency. In the decision-making process, company management requires relevant information about the essential components of business and technological processes, namely, every individual element within these processes that entails a financial outflow. The internal information system stores historical cost data, which forms part of a larger database established based on prior business experience. This database contains monetary amounts of costs paired with the corresponding expected performance or technological effect.

Cost management is an important element of ensuring economic security as it helps organizations control costs and optimize resource allocation. This is essential for maintaining financial stability in a competitive environment (Azimov, Hamidov, 2025). In recent times, cost accounting has been tasked with satisfying the diverse information needs of management (Vladisavljević, Vukosavljević, 2017). Practically, the use of management accounting information systems is limited to cost management, developing different types of budgets, and monitoring performance (Knežević et al., 2024). By applying new digital information technology tools, management accounting can provide quality information for strategic and operational decision-making (Spasić et al., 2024).

In economic theory, the importance of examining the interdependence between investments and the consumption of materials and energy is often emphasized as one of the key determinants in the creation of newly generated value (Beke Trivunac, Peković, 2025). Economic models are applied as instruments of analysis precisely because they enable solving a large number of economic problems arising from the effects of multiple variables (Pantić, et al., 2021). Achieving efficient cost management requires emphasizing agility. It is the ability to detect shifts in the environment and respond to them effectively (Lekić et al., 2023).

Predictive analytics has emerged as an essential instrument in strategic cost management, enabling companies to optimize pricing strategies and improve operational efficiency (Celestin, 2018). Cost accounting and budget preparation serve as foundational pillars of financial management, enabling organizations to allocate resources efficiently, control expenditures, and support strategic planning (Majumder, 2025). The application of business analytics can greatly improve the efficiency and impact of management accounting (Uyar, 2021). The different cost management and management control implications of service businesses deserve attention, as this area remains largely underexplored in the management accounting and control literature (Tkaczyk et al., 2025).

In addition to the identified demands for higher quality of transport services provided by transport companies, there is a persistent lack of financial resources. This most sought-after scarce resource today forces transport companies to optimize processes and associated resources while considering sometimes conflicting factors such as accessibility or availability, favorable pricing, and requirements for savings. Generating an adequate service offering is a demanding task for transport company management, which must always be carefully market-adjusted, with costs of each process structured within the product, i.e., the transport service, in focus.

At the micro level, when analyzing costs in transport companies, theorists observe that cost optimisation is crucial for efficiently managing overall company expenditures and represents the most important factor in achieving the desired financial results and further business development (Gerasimova, 2018). In assessing the market positions of transport companies, Gerasimova (2018) emphasizes that a company’s competitiveness primarily depends on the speed of adoption and application of various new concepts and technologies, resulting in higher-quality services at more affordable prices. With the development and strengthening of competition, companies’ profit margins decline, leaving proper cost management as the key measure. In this process, companies must strengthen their own capabilities and potential to retain or improve their market position. Cost rationalization requires the prevention of unnecessary, idle, or sunk costs, that is, those costs which, in essence, do not generate corresponding revenues.

Bokor (2009) notes shortcomings in calculating transport service prices, since business practice often relies excessively on arbitrary cost allocation keys. The most common pattern he identifies is the use of a universal average cost value such as “€/vehicle-km,” obtained by simply dividing the total incurred costs by work output. This approach does not account for cost differentiation factors, such as vehicle or service characteristics, which lead to inaccurate assessments of cost efficiency and business performance and ultimately result in inadequate resource allocation (Bokor, 2009).

As a significant driver of total operating costs, transportation costs directly affect pricing decisions, product competitiveness, and the overall business performance (Savić et al., 2020). In his study, Bokor (2009), analyzing transport costs at the micro level, examines the structure of operating costs, cost drivers, and the relationship between costs and performance, seeking solutions to the challenges of managing costs and performance. He highlights the benefits of improved cost and performance management for companies that are horizontally or vertically integrated, due to high ratios of indirect costs. Namely, when a certain resource is allocated and used for several distinct transport services, such costs cannot be easily attributed to a single service. For example, the main competitive advantages of road freight transport compared to other modes are its flexibility, reliability and fast delivery (Peštović et al., 2025).

Improving cost calculation in transport implies incorporating additional technologically oriented information, with the idea of allocating indirect costs to products based on the flows of technological processes rather than using ad hoc patterns. Bokor (2009) observes that a combination of technological and accounting data at least mitigates managerial ignorance resulting from the averaging of cost amounts in calculations. He proposes a general approach to transport cost calculation methodology that leverages technological performance indicators, which in turn enables the development of cost estimates for each service. By comparing the revenue from a service with its corresponding direct costs, the unit contribution margin is obtained. Companies can use this information for managerial decision- making and for accepting or rejecting certain market opportunities, relying on experiential methods and historical costs.

In contemporary business conditions, with a large number of competitors, companies must adapt to current market trends and offer new and unique services (products), while managing costs rationally, which increases the chances of business growth.

Effective cost management is a prerequisite for generating profit and expanding business operations through increased sales, growth in customer base, expansion into other markets, and domestic and foreign acquisitions. Bokor (2009) also points out that stronger competition fosters corporate integrations, i.e., mergers and acquisitions, and that such trends have been observed across all forms of transport (road, rail, and air).

Materials and methods

All statistical analyses were performed using IBM SPSS Statistics, version 22.0. Frequencies and percentages were used to describe the demographic and professional characteristics of respondents. For the questionnaire items measured on a five-point Likert scale, both frequency distributions (N and %) and measures of central tendency and variability were calculated. The reliability of the questionnaire and its subscales was assessed using Cronbach’s alpha coefficients. Group differences in total and subscale scores according to demographic and professional characteristics were examined using the Mann-Whitney U test and the Kruskal-Wallis test, with Bonferroni correction applied for multiple comparisons. Correlations between subscales and the overall score were analyzed using Spearman’s rho. Finally, multiple linear regression analysis was performed to examine predictors of the overall cost management score, with categorical variables entered into the model as dummy variables. Statistical significance was set at p<0.05.

Research results and discussion

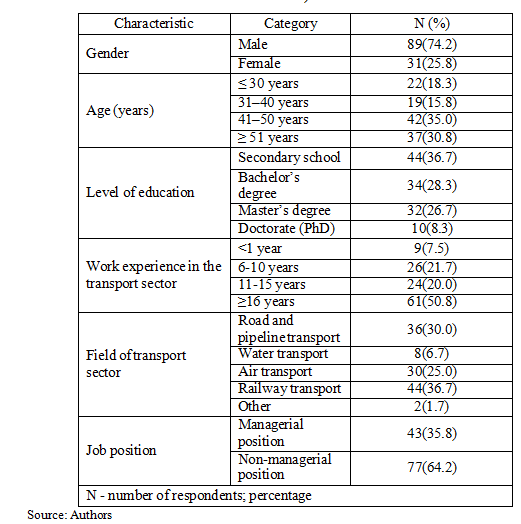

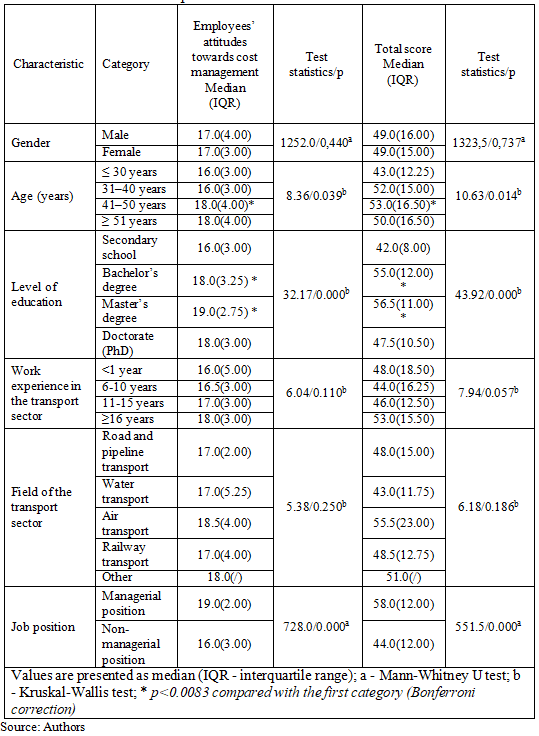

The research was conducted in the first half of 2025. A total of 120 respondents participated in this study, of whom 89 (74.2%) were male and 31 (25.8%) were female. The largest proportion of respondents was aged 41-50 years (42; 35.0%) and over 51 years (37; 30.8%). There were 22 respondents (18.3%) younger than 30 years, while 19 respondents (15.8%) were aged 31-40 years. Regarding education, most respondents had completed secondary school (44; 36.7%), followed by a bachelor’s degree (34; 28.3%) and a master’s degree (32; 26.7%), whereas 10 respondents (8.3%) held a doctorate (PhD). In terms of work experience in the transport sector, the majority had worked for 16 years or more (61; 50.8%), followed by 6-10 years (26; 21.7%) and 11-15 years (24; 20.0%), while the smallest group consisted of respondents with less than one year of experience (9; 7.5%). With respect to the field of transport, most respondents were employed in railway transport (44; 36.7%) and in road and pipeline transport (36; 30.0%), followed by air transport (30; 25.0%). Water transport accounted for 8 respondents (6.7%), while 2 respondents (1.7%) worked in other sectors. As for job positions, the majority of respondents were employed in non-managerial positions (77; 64.2%), while 43 respondents (35.8%) held managerial positions. Socio-demographic and professional characteristics of respondents are presented in Table 1.

Table 1. Socio-demographic and professional characteristics of respondents (N = 120)

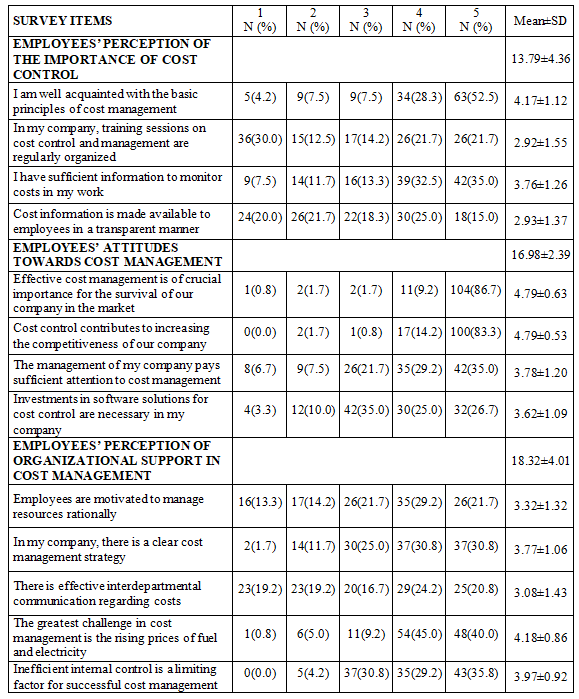

A questionnaire on cost management in transport companies, consisting of 13 items grouped into three subscales, was administered. The subscale Employees’ perception of the importance of cost control included four items, showing a mean total score of 13.79±4.36 (maximum 20), indicating a moderate level of agreement. The highest- rated statement was “I am well acquainted with the basic principles of cost management” (4.17±1.12), suggesting that employees possess solid knowledge of the fundamental principles of cost management. This was followed by “I have sufficient information to monitor costs in my work” (3.76±1.26), pointing to a generally positive perception of the availability of relevant information for cost monitoring. In contrast, the lowest-rated statements were “Cost information is made available to employees in a transparent manner” (2.93±1.37) and “In my company, training sessions on cost control and management are regularly organized” (2.92±1.55). These findings highlight organizational weaknesses in ensuring transparency of cost-related information and in implementing regular training programs on cost management. Overall, the results show that employees recognize the importance of cost control and see themselves as informed, while organizational support through transparent communication and regular training is still lacking.

Within the subscale Employees’ attitudes towards cost management, the mean total score was 16.98±2.39 (maximum 20), indicating a high level of agreement among respondents. The two highest-rated statements were “Effective cost management is of crucial importance for the survival of our company in the market” (4.79±0.63) and “Cost control contributes to increasing the competitiveness of our company” (4.79±0.53), both of which reflect employees’ strong recognition of cost management as a key factor for business survival and competitiveness. Lower scores were observed for the statements “The management of my company pays sufficient attention to cost management” (3.78±1.20) and “Investments in software solutions for cost control are necessary in my company” (3.62±1.09). These results show that employees recognize the strategic role of cost management but are less convinced that management gives it enough priority or invests in tools such as software solutions.

Analysis of the subscale Employees’ perception of organizational support in cost management, the mean total score was 18.32±4.01 (maximum 25), which points to a moderate to high level of agreement. The highest-rated statement was “The greatest challenge in cost management is the rising prices of fuel and electricity” (4.18±0.86), followed by “Inefficient internal control is a limiting factor for successful cost management” (3.97±0.92), which suggests that employees see external market conditions and weaknesses in internal control as the main obstacles to efficient cost management. Slightly lower scores were recorded for “In my company, there is a clear cost management strategy” (3.77±1.06), suggesting that while many employees recognize the existence of a strategy, not all are equally confident in its clarity. The lowest-rated statements were “Employees are motivated to manage resources rationally” (3.32±1.32) and “There is effective interdepartmental communication regarding costs” (3.08±1.43), which indicate that motivation and communication are perceived as weaker elements of organizational support. Overall, the findings suggest that employees identify external cost pressures and internal control as key factors, while aspects such as motivation and communication require further improvement.

Distribution of responses and mean scores for subscales of cost management in transport companies are presented in Table 2.

Table 2. Distribution of responses and mean scores for subscales of cost management in transport companies

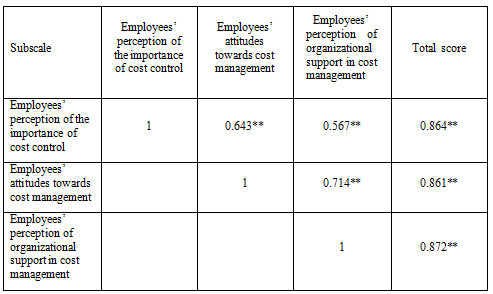

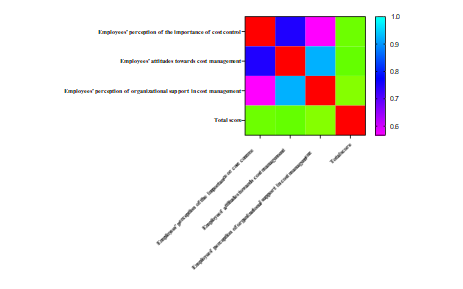

By summing all items, a total score was obtained with a mean value of 49.10±9.21, ranging from 29 to 65 points (out of a maximum possible 65). The results show that all subscales significantly and positively correlate with each other, as well as with the total score (p<0.01). The strongest correlation was observed between the subscale Employees’ perception of organizational support in cost management and the total score (ρ=0.872). This suggests that employees who report higher levels of organizational support, such as clear strategies, effective communication, and efficient internal control, also tend to achieve higher overall scores in cost management. Similarly, a very strong correlation was noted between Employees’ attitudes towards cost management and the total score (ρ=0.861), confirming that employees’ recognition of the strategic importance of cost management is in line with their overall responses. The lowest, but still strong, correlation was between Employees’ perception of the importance of cost control and Employees’ perception of organizational support in cost management (ρ=0.567). These results show clear connection between the three dimensions, indicating that employees’ knowledge, attitudes, and perceptions together shape the overall view of cost management in transport companies (Table 3, Figure 1). Since the total score was calculated as the sum of all subscales, the correlations between individual subscales and the total score should be interpreted with caution, as they are not fully independent. Nevertheless, these results provide useful insight into which dimensions contributed most strongly to the overall evaluation of cost management.

Table 3. Correlations between subscales and the overall score of employees’ statements and perceptions on cost management in transport companies

Figure 1. Heatmap of correlations between subscales and the overall score on cost management in transport companies

Cronbach’s alpha values indicated satisfactory internal consistency across all subscales: Employees’ perception of the importance of cost control (α=0.832; good reliability), Employees’ attitudes towards cost management (α=0.762; acceptable reliability), and Employees’ perception of organizational support in cost management (α=0.744; acceptable reliability). The overall score demonstrated good reliability (α=0.867). These results confirm that the subscales exhibit adequate internal consistency, indicating that the items within each subscale consistently measure the same dimension of cost management in transport companies.

Differences in the overall cost management score and the subscale Employees’ attitudes towards cost management were analyzed across demographic and professional characteristics. No significant gender differences were observed. Significant differences were found by age, showing the highest values among respondents aged 41-50 years and the lowest among those aged ≤30 years. Education level showed a clear upward trend, with significantly higher scores among respondents with bachelor’s or master’s degrees compared to those with secondary education. Work experience tended to be associated with higher scores in those with ≥16 years, but the differences were not significant. No significant differences were observed between transport sectors. In contrast, job position was significantly associated with both outcomes, with managerial staff reporting higher values compared to non-managerial employees. Results are presented in Table 4.

Table 4. Differences in the overall cost management score and the subscale Employees’ attitudes towards cost management across demographic and professional characteristics

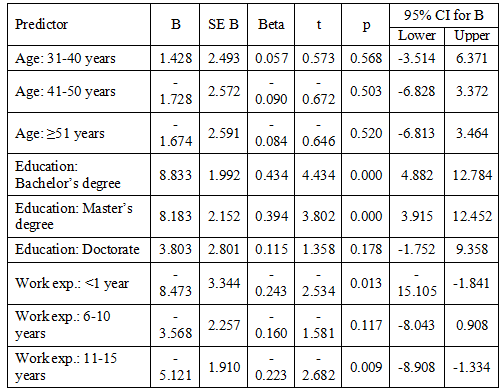

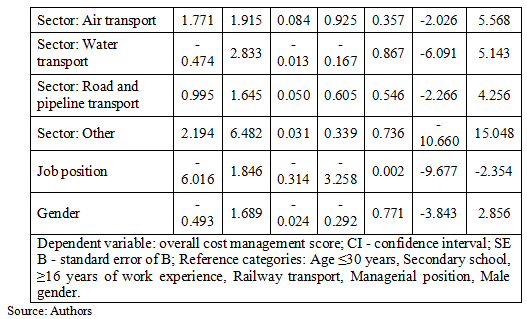

Multiple linear regression was conducted to examine the influence of demographic and professional characteristics on the overall cost management score. The overall model was statistically significant (F (15,104) = 7.094, p < 0.001), explaining 50.6% of the variance in the total score (R² = 0.506, Adjusted R² = 0.434). Respondents with a bachelor’s degree scored on average 8.83 points higher compared to those with secondary education (B = 8.83, p < 0.001). In comparison, those with a master’s degree scored 8.18 points higher (B = 8.18, p < 0.001), which indicates a clear positive effect of higher education on employees’ perceptions of cost management. Regarding work experience in the transport sector, respondents with less than one year of experience had significantly lower scores of 8.47 points compared to those with ≥16 years (B = -8.47, p < 0.05). Similarly, those with 11-15 years of experience scored 5.12 points lower than the reference group (B = -5.12, p< 0.05). This suggests that the longest-tenured employees reported more positive perceptions of cost management compared to those with shorter experience. The job position also showed a significant effect. Non-managerial employees scored on average 6.02 points lower than managerial employees (B = -6.02, p < 0.05), highlighting the importance of hierarchical position within organizations for shaping attitudes towards cost management. Other predictors, including gender, age, and field of transport sector, were not statistically significant (Table 5).

Table 5. Results of linear regression analysis with the overall cost management score as the dependent variable (N = 120)

In accordance with the formulated research questions, the following findings have been identified and are presented below.

The findings of this research indicate that employees largely recognize the relevance of cost control and believe they are familiar with its fundamental principles. Nevertheless, shortcomings in organizational transparency and the lack of regular training programs weaken the overall support provided to employees. Greater awareness and access to information were associated with stronger acknowledgement of the role of cost control. Clear differences were observed between managerial and non-managerial staff, with managers consistently achieving higher scores, which suggests that job position and proximity to decision-making significantly shape perceptions of cost management. Non-managerial employees showed lower values, pointing to the need for broader engagement across all organizational levels. Furthermore, employees identified rising energy costs and weaknesses in internal control as key barriers to effective cost management, while motivation and interdepartmental communication were recognized as weaker aspects of organizational support. The strong association between this subscale and the overall score confirms that clear strategies, modern tools, and effective communication channels play an essential role in shaping employees’ views on efficiency. Taking together, the results demonstrate that cost management in transport companies depends on the interplay of employees’ knowledge, attitudes, and the level of organizational support. Higher education, longer work experience, and managerial roles emerged as significant predictors of higher scores, emphasizing the importance of continuous professional development, transparent communication, and active participation of staff at all levels as a basis for strengthening cost management practices and maintaining competitiveness.

Conclusion

The paper studied the issue of employees’ perceptions regarding cost management practices in transport companies, with a focus on understanding how organizational communication, transparency, and employee characteristics influence attitudes toward cost control. The paper identifies the key determinants that can guide managers in making more informed business and financial decisions to achieve efficient cost management, while also providing valuable insights for policymakers in the transport economy sector.

In the globalization of the economy that has gained momentum, due to the relocation of world production to geographically distant locations, transport costs are increasingly recognized as a significant factor of competitiveness. They are the subject of study by theorists of trade economics, but also by researchers of global supply chains, where the consolidation of business and the struggle for a monopoly in the transport of goods market are observed. This is precisely where lies the key that can accelerate the advancement of the global production force from the East, towards the leader position of the world economy.

Reference

2.Anderson, J. E., and Wincoop, E. V. 2004. Trade costs. Journal of Economic Literature, 42: 691–751.

3.Azimov, B., & Hamidov, A. 2025. Theoretical and practical aspects of managing organizational costs in the economic security system. Journal of Applied Science and Social Science, 1: 356-363.

4.Beke Trivunac, J., & Peković, D. 2025. Učinak novih ulaganja na troškove

materijala i energije u privredi Republike Srbije. Oditor, 11: 169-

206. https://doi.org/10.59864/Oditor82501JBT

5.Bokor, Z. 2009. Elaborating on cost and performance management methods in transport. Traffic Management Review, 21: 217–224.

6.Camison-Haba, S., and Clemente-Almendros, J. A. 2020: A global model for the estimation of transport costs. Economic Research – Ekonomska istraživanja, 33: 2075–2100.

7.Celestin, M. 2018. Predictive analytics in strategic cost management: How companies use data to optimize pricing and operational efficiency. Brainae Journal of Business, Sciences and Technology (BJBST), 2: 706-717.

8.Chow, G., and Gill, V. 2011. Transportation and logistics international competitiveness: How does Canada fare? (pp. 5–23). Canada: Canadian Transportation Research.

9.Dan, H. (2022). Research on the problems of enterprise logistics transportation cost management and optimization countermeasures. SHS Web of Conferences, 148, 02006. ICPRSS 2022. https://doi.org/10.1051/shsconf/202214802006

10.Davis, H. W., and Drumm, W. H. 2002. Logistics costs and service database. In Annual Conference Proceedings of the Council of Logistics Management, San Francisco.

11.De, P. (2006, April). Why trade costs matter? (Working Paper No. 7). Bangkok, Thailand: Asia–Pacific Research and Training Network on Trade.

12.Djankov, S., Freund, C., and Pham, C. S. 2010. Trading on time. The Review of Economics and Statistics, 92: 166–173.

13.Gerasimova, L. 2018. Cost accounting in transport companies. MATEC Web of Conferences, 239, 08019. TransSiberia. https://doi.org/10.1051/matecconf/201823908019

14.Glaser, E. L., & Kohlhase, J. E. 2004. Cities, regions and the decline of transport costs. Papers in Regional Science, 83: 197–228.

15.Gregor, T., Krajčovič, M., and Wiecek, D. 2017. Smart connected logistics. In TRANSCOM 2017: International Scientific Conference on Sustainable, Modern and Safe Transport. Procedia Engineering, 192: 265–270.

16.Hummels, D. 2007. Transportation costs and international trade in the second era of globalization. Journal of Economic Perspectives, 21: 131–154.

17.International Monetary Fund (IMF). 2016. World economic outlook: Subdued demand: Symptoms and remedies. Washington, DC: IMF.

18.Knežević, S., Milojević, S., Mitrović, A., & Trivunac, J. B. 2024. Računovodstvo troškova kao podrška sistemu upravljanja životnom sredinom Cost accounting as a support for the environmental management system. Ecologica, 31: 58-66.

19.Kufel, M. 1990. Koszty przepływy materiałów w przedsiębiorstwach przemysłowych. Problemy budżetowania, ewidencji i kontroli. AE, Wrocław.

20.Kwejt, J. 1982. Zaopatrzenie i gospodarka materiałowa. Państwowe

Wydawnictwo Ekonomiczne, Warszawa.

21.Lekić, N., Vapa-Tankosić, J., Mirjanić, B., & Lekić, S. 2023. Uticaj organizacionih parametara na poslovnu agilnosti informatičkih preduzeća Republike Srbije [Impact of Organizational Parameters on the Business Agility of IT Companies in the Republic of Serbia]. Akcionarstvo, 29: 181-198.

22.Majumder, Ruhul Quddus, Impact of Technological Advancements on Cost Accounting Practices and Budget Preparation (April 17, 2025). Available at SSRN: https://ssrn.com/abstract=5357971 or http://dx.doi.org/10.2139/ssrn53 57971

23.Micco, A., and Perez, N. 2002. Determinants of maritime transport costs (Working Paper No. 441). Washington, DC: Inter-American Development Bank, Research Department.

24.Miljković, M., and Nikolić, I. 2024. The role of the transportation sector in

Serbia’s macroeconomic performances. Industrija, 52: 7–20.

25.Milojević, S., Knežević, S., Grivec, M., and Đokić, O. 2024. Upravljanje troškovima zdravstvenih organizacija za finansijsku održivost. Revizor - Časopis za upravljanje organizacijama, finansije i reviziju, 27: 47–59.

26.Nowakowska-Grunt, J. 2013. Strategies for enterprises of logistics market in Poland and Europe. In Proceedings of the International Scientific and Practical Conference: Strategy of the Enterprise - Change of the Management Paradigm and Innovative Business Solutions. Kyiv National Economic University.

27.Pantić, N., Damnjanović, R., & Kostić, R. 2021. Metod ekonomske analize kao deo metoda društvenih nauka. Akcionarstvo, 27: 7-26.

28.Peštović, K., Nuševa, D., Dakić, S., & Đurković Marić, T. 2025. Analysis of the profitability of road freight transport in the Republic of Serbia, DOI: 10.5937/etp240424P. Ekonomija - Teorija i praksa, 17: 24–40. Retrieved from https://casopis.fimek.edu.rs/index.php/etp/article/view/313

29.Pešut, M. 2009. Global supply chains, transport and competitiveness. Geneva: United Nations Economic Commission for Europe.

30.Pfohl, H.C. 2022. Importance of Logistics. In: Logistics Systems. Berlin, Heidelberg: Springer

31.Radelet, S., and Sachs, J. 1998. Shipping costs, manufactured exports and economic growth. Washington, DC: World Bank Group.

32.Savić, B., Petrović, M., & Vasiljević, Z. 2020. The impact of transportation costs on economic performances in crop production. Economic of Agriculture, 67: 683–697. https://doi.org/10.5937/ekoPolj2003683S

33.Skowron-Grabowska, B. 2014. Innovation of logistics processes. Vysoká škola báňská – Technical University of Ostrava.

34.Spasić, K., Čečević, B. N., & Antić, L. 2024. The impact of digitization of the cost accounting system on organizational efficiency and effectiveness in the healthcare sector of the Republic of Serbia. BizInfo Blace, 15: 39-47.

35.Srebro, B., Mavrenski, B., Bogojević Arsić, V., Knežević, S., Milašinović. M., Travica, J. 2021. Bankruptcy Risk Prediction in Ensuring the Sustainable Operation of Agriculture Companies. Sustainability. 13: 7712.

36.Stalmašeková, N., Genzorová, T., Čorejová, T., Gašperová, L. 2017. The impact of using the digital environment in transport. In TRANSCOM 2017: International Scientific Conference on Sustainable, Modern and Safe Transport. Procedia Engineering, 192: 231–236.

37.Stępień, M., Legowik-Świącik, S., Skibińska, W., and Turek, I. 2016. Identification and measurement of logistic cost parameters in the company. Transportation Research Procedia, 16: 490–497.

38.Szałek, B. 1994. Logistyka: Wstęp do problematyki. Uniwersytet Szczeciński,

Szczecin.

39.Tkaczyk, M., Salina, A., Lyly-Yrjänäinen, J., & Laine, T. 2025. Towards a digital twin of a service: a case of communicating cost and control implications of a new after-sales service with an animation. Qualitative Research in Accounting & Management, 22: 230-255.

40.United Nations Conference on Trade and Development. (2015). Review of maritime transport 2015. United Nations Publications..

41.Uyar, M. 2021. The role of business analytics in transforming management accounting information into cost performance. Ege Academic Review, 21: 373- 389.

42.Vladisavljević, V., & Vukasović, B. 2017. Savremeni sistemi obračuna troškova. Oditor, 3: 133-151.

43.World Trade Organization (WTO). (2013). Annual report 2013. Geneva: World Trade Organization.

44.Zamora, A., & Pedraza, O. H. 2013. El transporte internacional como factor de competitividad en el comercio exterior. Journal of Economics, Finance and Administrative Science, 18: 108–118.

45.Zeng, A. Z., & Rossetti, C. 2003. Developing a framework for evaluating logistics costs in the global sourcing process: Implementation and insights. International Journal of Physical Distribution & Logistics Manage

Objavljeno u

God. 11 Br. 3 (2025)

Ključne reči

🛡️ Licenca i prava korišćenja

Ovaj rad je objavljen pod Creative Commons Attribution 4.0 International (CC BY 4.0).

Autori zadržavaju autorska prava nad svojim radom.

Dozvoljena je upotreba, distribucija i adaptacija rada, uključujući i u komercijalne svrhe, uz obavezno navođenje originalnog autora i izvora.

Zainteresovani za slična istraživanja?

Pregledaj sve članke i časopise